13. Heston Model: Hedging Under Stochastic Volatility#

Extends the BS hedging analysis to Heston. The main questions:

What happens when you hedge with BS deltas but reality follows Heston?

Does using the “correct” Heston delta actually help?

What risk can’t you hedge away with stock alone?

13.1. Heston Model Recap#

Under Heston [Heston, 1993], stock and variance follow:

with \(\text{Corr}(dW^S, dW^v) = \rho\).

The parameters: \(v_0\) is initial variance, \(\theta\) is long-run variance, \(\kappa\) controls mean-reversion speed, \(\xi\) is vol-of-vol, and \(\rho\) is typically negative (the leverage effect—when stock drops, vol tends to rise).

For hedging, the key difference from BS is that volatility is now a second source of randomness. Option prices depend on the current vol level, and that level moves around.

Model Parameters

========================================

Spot S0: 100

Strike K: 100

Time T: 0.25 years

Risk-free r: 0.05

Initial vol: 20.0%

Long-run vol: 20.0%

Vol-of-vol xi: 0.3

Correlation rho: -0.7

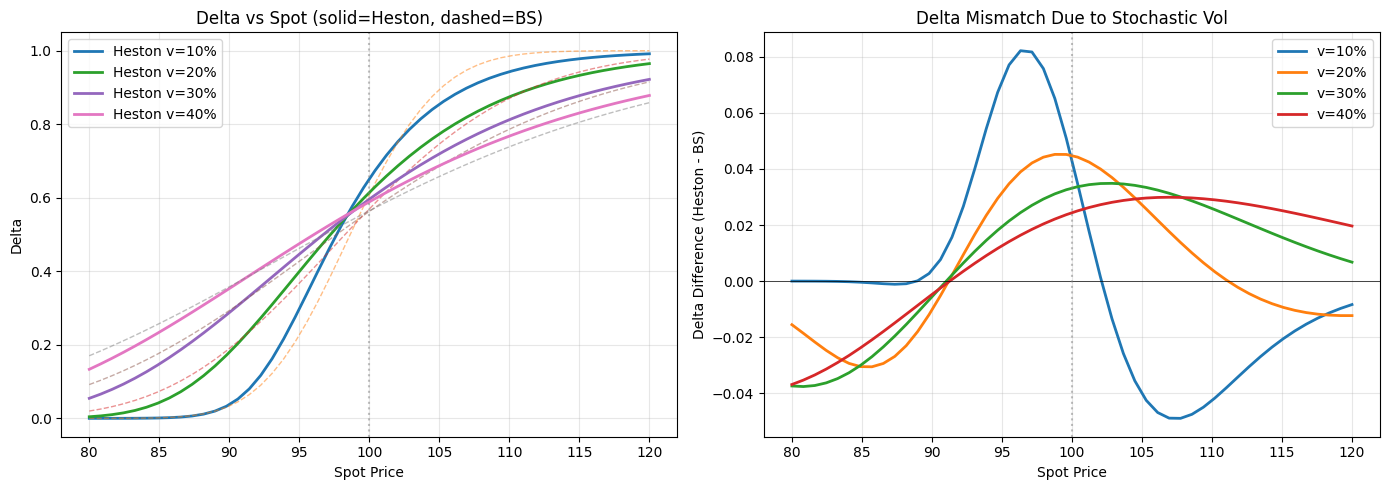

13.2. Heston Greeks via COS Method#

Under Heston, Greeks need to be computed numerically. We use the COS method [Fang and Oosterlee, 2008]—analytical derivatives for delta/gamma, finite differences for vega and theta.

The important difference from BS: Heston delta depends on the current variance \(v_t\), not just spot. Even if spot doesn’t move, delta changes as vol moves around.

Greeks Comparison: BS vs Heston

==================================================

Greek BS Heston Diff %

--------------------------------------------------

Price 4.614997 4.587070 -0.61%

Delta 0.569460 0.614251 7.87%

Gamma 0.039288 0.038115 -2.99%

Theta -10.474151 -10.361430 1.08%

Vega 19.644000 15.375729 -21.73%

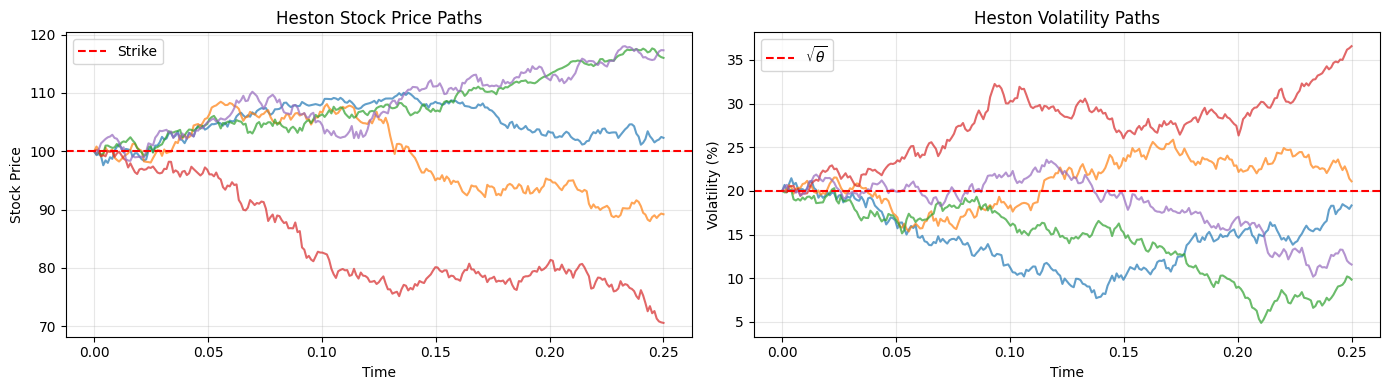

13.3. Simulating Heston Paths#

We use Euler discretization:

where \(Z_1\) and \(Z_2\) are correlated normals with \(\text{Corr}(Z_1, Z_2) = \rho\).

13.4. BS Delta vs Heston Delta#

Here’s the experiment: reality follows Heston, we sell an option and delta-hedge. We compare hedging with BS delta (using \(\sigma = \sqrt{v_t}\)) vs the full Heston delta.

Both methods observe the true variance at each hedge time. The question is whether knowing the full Heston dynamics—mean-reversion, vol-of-vol, correlation—actually improves the hedge.

We expect the unhedgeable vol risk to dominate the delta choice — let’s see.

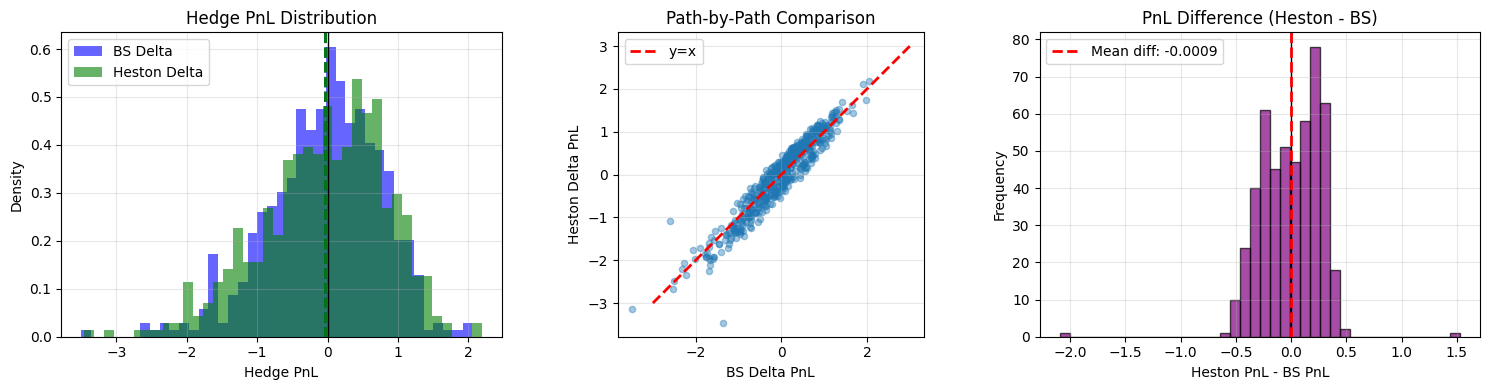

Running hedge comparison...

Hedge PnL Statistics

============================================================

Metric BS Delta Heston Delta

------------------------------------------------------------

Mean PnL -0.0424 -0.0433

Std PnL 0.8005 0.8826

5th Percentile -1.5596 -1.6255

95th Percentile 1.1424 1.1698

Key Finding:

BS Delta std: 0.8005

Heston Delta std: 0.8826

Correlation: 0.9530

The high correlation shows both methods face the SAME underlying risk: vol moves.

PnL from both methods is highly correlated — the unhedgeable vol risk dominates the delta choice. Model choice matters more for exotics with strong path-dependence.

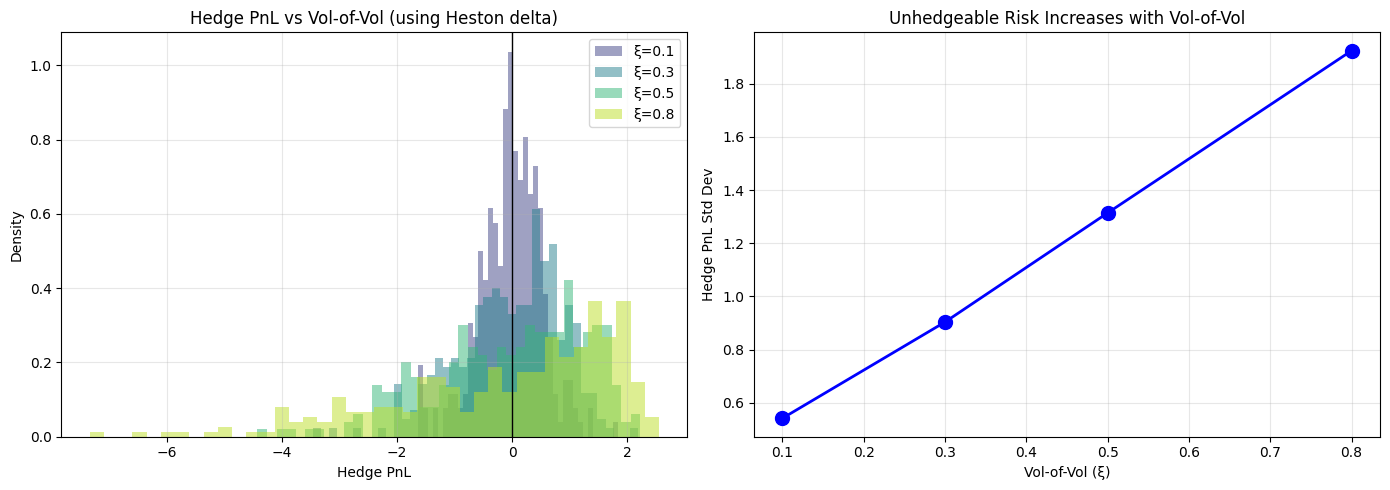

13.5. The Unhedgeable Risk: Vol-of-Vol#

Even with the correct Heston delta, risk remains. The option value depends on two state variables, \(V = V(S_t, v_t, t)\), and the delta-hedged PnL is:

Stock hedges the \(dS\) risk. But the \(dv\) term—exposure to variance moves—requires other instruments: variance swaps, VIX options, or other vanilla options.

With only stock, the \(dv\) exposure remains. And this exposure scales with \(\xi\) (vol-of-vol): higher \(\xi\) means more variance in variance, means more unhedgeable risk.

Testing vol-of-vol impact...

xi=0.1: std=0.5416

xi=0.3: std=0.9037

xi=0.5: std=1.3142

xi=0.8: std=1.9244

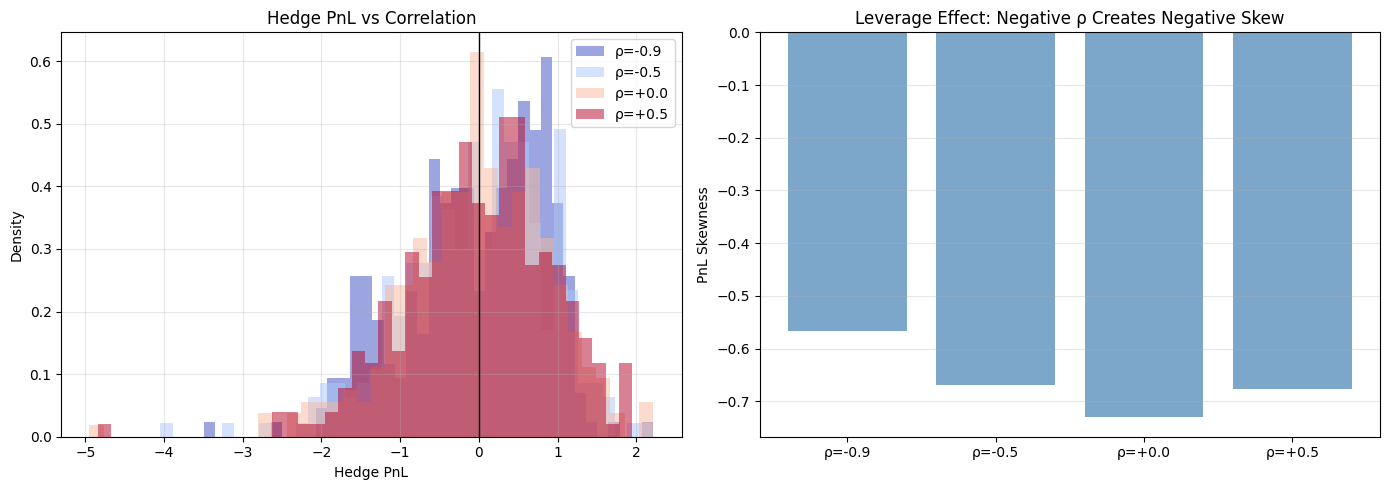

13.6. The Leverage Effect#

The correlation \(\rho\) between stock returns and variance creates the leverage effect: when stock drops, vol tends to rise (\(\rho < 0\)). This creates negatively-skewed returns—the left tail is fatter.

For hedging, this is bad news. Large down moves coincide with vol spikes, so your hedge deteriorates exactly when you need it most. The PnL distribution becomes negatively skewed.

Testing correlation impact...

rho=-0.9: mean=-0.0420, std=0.8852

rho=-0.5: mean=-0.0362, std=0.9147

rho=+0.0: mean=-0.0349, std=0.9318

rho=+0.5: mean=-0.0146, std=0.9282

For vanilla hedging, BS delta with current vol works nearly as well as Heston delta. The dominant risk is vol moves, which stock can’t hedge — need variance swaps or other options for that.

TODO: add vega hedging with a second option to quantify how much residual risk drops.