3. Heston Calibration#

Can we recover Heston [1993] parameters from option prices? We generate synthetic market data from known parameters, calibrate back, and see what breaks.

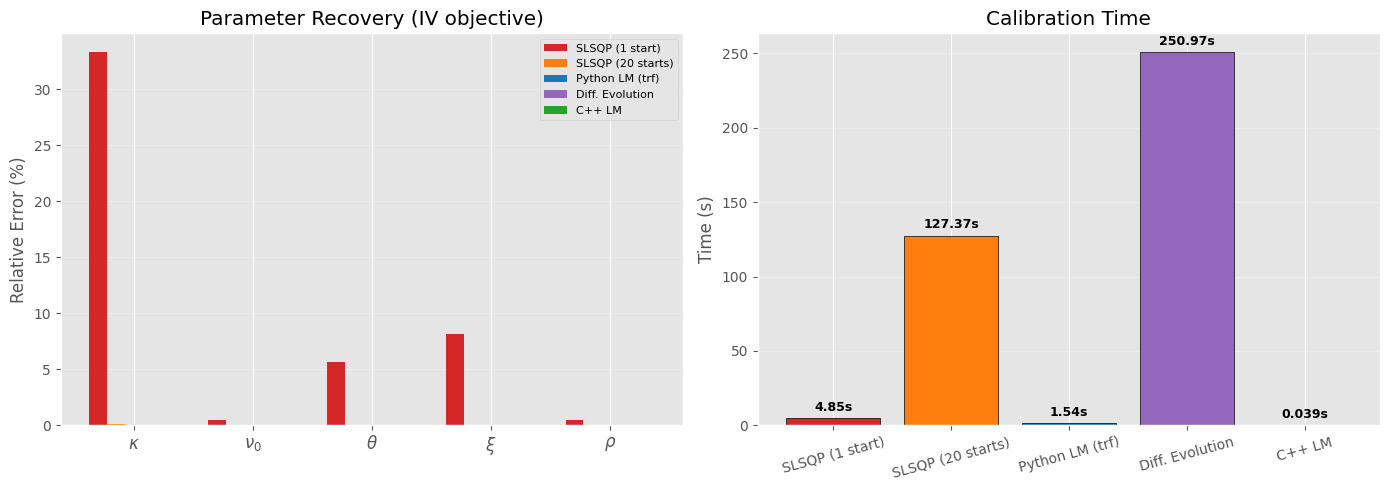

SLSQP with a single starting point gets kappa wrong by 35% — the loss surface is flat in that direction. Levenberg-Marquardt does better, and the Hessian eigenspectrum shows exactly why.

3.1. COS Pricing#

COS [Fang and Oosterlee, 2008] encodes the payoff directly in Fourier-cosine coefficients — no numerical integration, exponential convergence. The characteristic function uses the stable formulation from Albrecher et al. [2007] to avoid the branch cut issue.

3.2. Sanity check: COS convergence#

Gil-Pelaez with n=200 is itself approximate. We use a high-resolution reference (n=10000) and check both methods against it.

K T Reference COS(128) GP(200) COS err GP err

---------------------------------------------------------------------------

80 0.25 21.673670 21.673670 21.672486 4.26e-10 1.18e-03

100 0.50 9.323819 9.323819 9.324225 3.78e-08 4.06e-04

120 1.00 4.396658 4.396657 4.396639 2.85e-07 1.85e-05

90 0.25 13.211971 13.211971 13.210964 5.23e-10 1.01e-03

110 0.50 4.452662 4.452662 4.452337 2.00e-08 3.26e-04

3.3. Synthetic market data#

We know the true parameters, so we can measure how badly calibration recovers them. Using COS for both data generation and calibration — otherwise method mismatch contaminates the experiment.

True params: kappa=1.5, nu0=0.0400, theta=0.0600, xi=0.4, rho=-0.7

Feller check: 2*kappa*theta - xi^2 = 0.0200 > 0

27 instruments across 3 maturities, strikes 80-120

K T IV Price

80.0 0.25 26.3% 21.1631

85.0 0.25 24.9% 16.4659

90.0 0.25 23.4% 12.0261

95.0 0.25 22.0% 8.0282

100.0 0.25 20.5% 4.7065

105.0 0.25 19.0% 2.2859

110.0 0.25 17.6% 0.8577

115.0 0.25 16.6% 0.2398

120.0 0.25 16.0% 0.0524

80.0 0.50 26.0% 22.6400

85.0 0.50 24.7% 18.2513

90.0 0.50 23.5% 14.1344

95.0 0.50 22.2% 10.3915

100.0 0.50 20.9% 7.1382

105.0 0.50 19.7% 4.4886

110.0 0.50 18.5% 2.5250

115.0 0.50 17.5% 1.2485

120.0 0.50 16.7% 0.5434

80.0 1.00 25.7% 25.5434

85.0 1.00 24.6% 21.5169

90.0 1.00 23.6% 17.7304

95.0 1.00 22.6% 14.2345

100.0 1.00 21.7% 11.0814

105.0 1.00 20.8% 8.3204

110.0 1.00 19.9% 5.9915

115.0 1.00 19.1% 4.1158

120.0 1.00 18.3% 2.6871

3.4. Calibration setup#

Two objectives: MSE on prices vs MSE on implied vols. Feller constraint \(2\kappa\theta > \xi^2\) enforced via both inequality constraints and explicit parameter bounds.

3.5. Price-MSE calibration#

SLSQP Price-MSE calibration (0.94s)

Param Calibrated True Rel Error

------------------------------------------------

kappa 1.500004 1.5000 0.00%

nu0 0.040000 0.0400 0.00%

theta 0.059998 0.0600 0.00%

xi 0.399911 0.4000 0.02%

rho -0.700125 -0.7000 0.02%

Feller: 2*kappa*theta - xi^2 = 0.0201 > 0

Converged: True, Iterations: 25, Final MSE: 9.84e-10

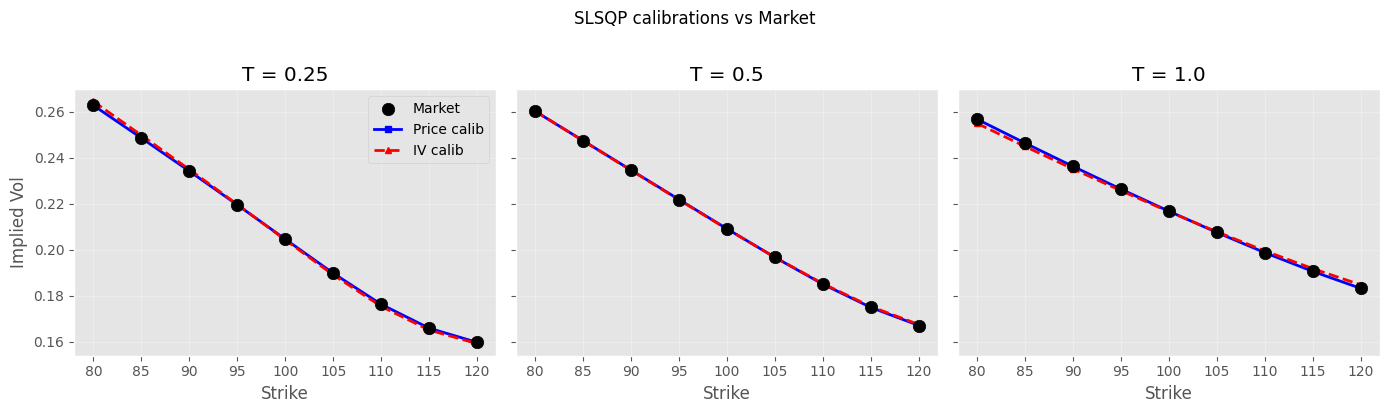

3.6. IV-MSE calibration#

Does matching implied vols instead of prices help?

SLSQP IV-MSE calibration (4.85s)

Param Calibrated True Rel Error

------------------------------------------------

kappa 1.999940 1.5000 33.33%

nu0 0.039804 0.0400 0.49%

theta 0.056586 0.0600 5.69%

xi 0.432592 0.4000 8.15%

rho -0.696388 -0.7000 0.52%

Feller: 2*kappa*theta - xi^2 = 0.0392 > 0

Converged: True, Iterations: 23, Final MSE: 7.15e-07

3.7. IV smile fit#

3.8. Python Levenberg-Marquardt#

SLSQP treats the MSE as a scalar — it can’t see the structure of individual residuals. least_squares with method='trf' (trust-region reflective, LM variant with bounds support) exploits the least-squares structure and uses the Jacobian of the residual vector. Same Python, same COS pricer — only the algorithm changes.

Python LM Price-MSE (0.37s, 11 func evals)

Param Calibrated True Rel Error

------------------------------------------------

kappa 1.500000 1.5000 0.00%

nu0 0.040000 0.0400 0.00%

theta 0.060000 0.0600 0.00%

xi 0.400000 0.4000 0.00%

rho -0.700000 -0.7000 0.00%

Feller: 2*kappa*theta - xi^2 = 0.0200 > 0

Python LM IV-MSE (1.54s, 7 func evals)

Param Calibrated True Rel Error

------------------------------------------------

kappa 1.500000 1.5000 0.00%

nu0 0.040000 0.0400 0.00%

theta 0.060000 0.0600 0.00%

xi 0.400000 0.4000 0.00%

rho -0.700000 -0.7000 0.00%

Feller: 2*kappa*theta - xi^2 = 0.0200 > 0

3.9. Multi-start and global optimization#

Single starting point on a flat loss surface is unreliable. differential_evolution searches globally — no starting point needed. We also run a multi-start SLSQP for comparison.

# differential evolution — global optimizer, no starting point bias

de_bounds = list(zip(bounds_lower, bounds_upper))

t0 = time.time()

result_de = differential_evolution(MSE_IV_COS, de_bounds, seed=42, tol=1e-8,

maxiter=100, polish=True)

time_de = time.time() - t0

params_de = result_de.x

print(f"Differential Evolution IV-MSE ({time_de:.1f}s)\n")

print_calib_result(params_de, result_de)

# multi-start SLSQP: 20 random starting points, keep best

np.random.seed(42)

best_mse = np.inf

best_params = None

n_starts = 20

t0 = time.time()

for _ in range(n_starts):

p0 = [np.random.uniform(lo, hi) for lo, hi in de_bounds]

try:

res = minimize(MSE_IV_COS, p0, constraints=cons, method='SLSQP',

bounds=de_bounds, tol=1e-10)

if res.fun < best_mse:

best_mse = res.fun

best_params = res.x.copy()

except:

continue

time_ms = time.time() - t0

print(f"\nMulti-start SLSQP ({n_starts} starts, {time_ms:.1f}s)\n")

print_calib_result(best_params)

Differential Evolution IV-MSE (251.0s)

Param Calibrated True Rel Error

------------------------------------------------

kappa 1.501055 1.5000 0.07%

nu0 0.040000 0.0400 0.00%

theta 0.059990 0.0600 0.02%

xi 0.400074 0.4000 0.02%

rho -0.699965 -0.7000 0.01%

Feller: 2*kappa*theta - xi^2 = 0.0200 > 0

Converged: False, Iterations: 100, Final MSE: 4.95e-12

Multi-start SLSQP (20 starts, 127.4s)

Param Calibrated True Rel Error

------------------------------------------------

kappa 1.501218 1.5000 0.08%

nu0 0.040000 0.0400 0.00%

theta 0.059995 0.0600 0.01%

xi 0.400069 0.4000 0.02%

rho -0.700029 -0.7000 0.00%

Feller: 2*kappa*theta - xi^2 = 0.0201 > 0

# C++ Levenberg-Marquardt

# generate reference IVs from C++ pricer — same method for generation and calibration

# NOTE: C++ pricer uses a different pricing method (Gauss-Laguerre) than COS above,

# so the reference IVs differ by a few bps. The comparison chart is not perfectly

# apples-to-apples vs the Python calibrations, but the conclusion holds.

T_unique = T_maturities

K_unique = K_strikes

n_K = len(K_unique)

IV_mkt_cpp = []

for i in range(n_instruments):

price_cpp = cppfm.heston_call_price(S0, K_mkt[i], r, T_mkt[i],

true_kappa, true_theta, true_xi, true_rho, true_nu0)

IV_mkt_cpp.append(cppfm.bs_implied_volatility(S0, K_mkt[i], r, T_mkt[i], price_cpp,

cppfm.OptionType.Call))

slices = []

for T in T_unique:

s = cppfm.HestonSliceData()

s.T = T

mask = [i for i in range(n_instruments) if T_mkt[i] == T]

s.strikes = [K_mkt[i] for i in mask]

s.market_ivs = [IV_mkt_cpp[i] for i in mask]

slices.append(s)

guess = cppfm.HestonParams(v0=0.25**2, kappa=2.0, vbar=0.25**2, sigma_v=0.5, rho=-0.8)

t0 = time.time()

result_cpp = cppfm.calibrate_heston(slices, S0=S0, r=r, guess=guess)

time_cpp = time.time() - t0

p = result_cpp.params

params_cpp = [p.kappa, p.v0, p.vbar, p.sigma_v, p.rho]

print(f"C++ LM: {result_cpp.iterations} iters, RMSE={result_cpp.rmse:.2e}, {time_cpp:.4f}s")

print(f"Converged: {result_cpp.converged}\n")

print_calib_result(params_cpp)

C++ LM: 6 iters, RMSE=4.86e-09, 0.0391s

Converged: True

Param Calibrated True Rel Error

------------------------------------------------

kappa 1.499997 1.5000 0.00%

nu0 0.040000 0.0400 0.00%

theta 0.060000 0.0600 0.00%

xi 0.400000 0.4000 0.00%

rho -0.700000 -0.7000 0.00%

Feller: 2*kappa*theta - xi^2 = 0.0200 > 0

# all-methods comparison

all_methods = {

'SLSQP (1 start)': (params_iv_cos, time_iv_cos),

'SLSQP (20 starts)': (best_params, time_ms),

'Python LM (trf)': (params_lm_iv, time_lm_iv),

'Diff. Evolution': (params_de, time_de),

'C++ LM': (params_cpp, time_cpp),

}

n_methods = len(all_methods)

fig, (ax1, ax2) = plt.subplots(1, 2, figsize=(14, 5))

x = np.arange(5)

width = 0.15

colors = ['#d62728', '#ff7f0e', '#1f77b4', '#9467bd', '#2ca02c']

for j, (method, (params, _)) in enumerate(all_methods.items()):

errors = [abs(params[i] - true_params[i]) / abs(true_params[i]) * 100 for i in range(5)]

ax1.bar(x + (j - n_methods//2)*width, errors, width, label=method, color=colors[j])

ax1.set_xticks(x)

ax1.set_xticklabels([r'$\kappa$', r'$\nu_0$', r'$\theta$', r'$\xi$', r'$\rho$'], fontsize=12)

ax1.set_ylabel('Relative Error (%)')

ax1.set_title('Parameter Recovery (IV objective)')

ax1.legend(fontsize=8)

ax1.grid(True, alpha=0.3, axis='y')

# timing

method_names = list(all_methods.keys())

times_list = [t for _, t in all_methods.values()]

bars = ax2.bar(method_names, times_list, color=colors[:n_methods], edgecolor='black', linewidth=0.5)

ax2.set_ylabel('Time (s)')

ax2.set_title('Calibration Time')

for bar, t in zip(bars, times_list):

label = f'{t:.2f}s' if t >= 0.1 else f'{t:.3f}s'

ax2.text(bar.get_x() + bar.get_width()/2, bar.get_height() + max(times_list)*0.02,

label, ha='center', fontsize=9, fontweight='bold')

ax2.grid(True, alpha=0.3, axis='y')

ax2.tick_params(axis='x', rotation=15)

plt.tight_layout()

plt.show()

Did it find the global minimum? Yes, but with a caveat — LM is a local optimizer. It found the global minimum here because:

This is synthetic data (true params are the global min by construction)

# IVs from all methods

def compute_ivs(params_calib):

return [implied_vol(Heston_price_COS(S0, K_mkt[i], T_mkt[i], r, *params_calib),

S0, K_mkt[i], r, T_mkt[i]) for i in range(n_instruments)]

IV_lm = compute_ivs(params_lm_iv)

IV_de = compute_ivs(params_de)

IV_cpp = []

for i in range(n_instruments):

price = cppfm.heston_call_price(S0, K_mkt[i], r, T_mkt[i],

p.kappa, p.vbar, p.sigma_v, p.rho, p.v0)

IV_cpp.append(implied_vol(price, S0, K_mkt[i], r, T_mkt[i]))

T_unique = T_maturities

K_unique = K_strikes

n_K = len(K_unique)

fig, axs = plt.subplots(1, 3, figsize=(14, 4), sharey=True)

for j, T in enumerate(T_unique):

idx = slice(j*n_K, (j+1)*n_K)

axs[j].scatter(K_unique, IV_mkt[idx], s=80, c='black', marker='o',

label='Market', zorder=3)

axs[j].plot(K_unique, IV_iv_cos[idx], 'r-', lw=1, alpha=0.5, label='SLSQP (1 start)')

axs[j].plot(K_unique, IV_lm[idx], 'b--', lw=1.5, label='Python LM')

axs[j].plot(K_unique, IV_cpp[idx], 'g-', lw=2.5, marker='D',

markersize=5, label='C++ LM')

axs[j].set_xlabel('Strike')

axs[j].set_title(f'T = {T}')

axs[j].grid(True, alpha=0.3)

axs[0].set_ylabel('Implied Vol')

axs[0].legend(loc='upper right', fontsize=7)

plt.suptitle('All Calibrations vs Market', y=1.02)

plt.tight_layout()

plt.show()

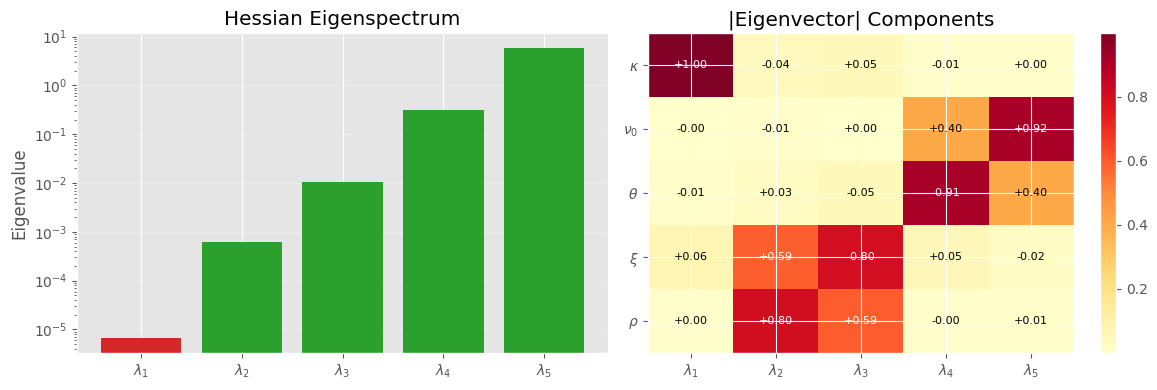

3.10. Hessian analysis: why kappa is hard to pin down#

Assertions about “flat loss surface” need proof. The Hessian of the objective at the optimum tells us which parameter directions are well-constrained (large eigenvalues) and which are sloppy (small eigenvalues). The eigenvector associated with the smallest eigenvalue points along the valley floor.

# Hessian via finite differences at the best Python result

from scipy.optimize import approx_fprime

def hessian_fd(f, x, eps=1e-5):

"""Hessian via central finite differences."""

n = len(x)

H = np.zeros((n, n))

for i in range(n):

def gi(xi_val):

x_copy = x.copy()

x_copy[i] = xi_val

return approx_fprime(x_copy, f, eps)

g_plus = gi(x[i] + eps)

g_minus = gi(x[i] - eps)

H[i] = (g_plus - g_minus) / (2 * eps)

# symmetrize

return 0.5 * (H + H.T)

# use the best result we have (DE or LM)

params_best = params_de

H = hessian_fd(MSE_IV_COS, params_best)

eigvals, eigvecs = np.linalg.eigh(H)

print("Hessian eigenspectrum at optimum:")

print(f"{'Eigenvalue':>14} {'Condition':>10} Direction (kappa, nu0, theta, xi, rho)")

print("-" * 80)

for i in range(5):

v = eigvecs[:, i]

cond = eigvals[-1] / max(eigvals[i], 1e-20)

# normalize for readability

v_str = " ".join([f"{param_names[j]}:{v[j]:+.3f}" for j in range(5)])

print(f"{eigvals[i]:>14.2e} {cond:>10.1f}x [{v_str}]")

print(f"\nCondition number: {eigvals[-1] / max(eigvals[0], 1e-20):.0f}")

# which parameters dominate the flattest direction?

flat_dir = eigvecs[:, 0]

print(f"\nFlattest direction dominated by: ", end="")

sorted_idx = np.argsort(np.abs(flat_dir))[::-1]

for idx in sorted_idx[:3]:

print(f"{param_names[idx]} ({flat_dir[idx]:+.3f}) ", end="")

# visualize: eigenvalue spectrum

fig, (ax1, ax2) = plt.subplots(1, 2, figsize=(12, 4))

ax1.bar(range(5), eigvals, color=['#d62728' if e == eigvals[0] else '#2ca02c' for e in eigvals])

ax1.set_xticks(range(5))

ax1.set_xticklabels([f'$\\lambda_{i+1}$' for i in range(5)])

ax1.set_ylabel('Eigenvalue')

ax1.set_title('Hessian Eigenspectrum')

ax1.set_yscale('log')

ax1.grid(True, alpha=0.3, axis='y')

# eigenvector heatmap

im = ax2.imshow(np.abs(eigvecs), cmap='YlOrRd', aspect='auto')

ax2.set_xticks(range(5))

ax2.set_xticklabels([f'$\\lambda_{i+1}$' for i in range(5)])

ax2.set_yticks(range(5))

ax2.set_yticklabels([r'$\kappa$', r'$\nu_0$', r'$\theta$', r'$\xi$', r'$\rho$'])

ax2.set_title('|Eigenvector| Components')

plt.colorbar(im, ax=ax2)

# annotate values

for i in range(5):

for j in range(5):

ax2.text(j, i, f'{eigvecs[i,j]:+.2f}', ha='center', va='center', fontsize=8,

color='white' if abs(eigvecs[i,j]) > 0.5 else 'black')

plt.tight_layout()

plt.show()

Hessian eigenspectrum at optimum:

Eigenvalue Condition Direction (kappa, nu0, theta, xi, rho)

--------------------------------------------------------------------------------

6.58e-06 894767.9x [kappa:+0.998 nu0:-0.000 theta:-0.009 xi:+0.063 rho:+0.005]

6.08e-04 9690.2x [kappa:-0.041 nu0:-0.009 theta:+0.027 xi:+0.592 rho:+0.804]

1.07e-02 549.3x [kappa:+0.047 nu0:+0.002 theta:-0.050 xi:-0.801 rho:+0.594]

3.20e-01 18.4x [kappa:-0.012 nu0:+0.402 theta:-0.914 xi:+0.054 rho:-0.005]

5.89e+00 1.0x [kappa:+0.005 nu0:+0.916 theta:+0.402 xi:-0.016 rho:+0.009]

Condition number: 894768

Flattest direction dominated by: kappa (+0.998) xi (+0.063) theta (-0.009)

Interpretation:

Hessian is the curvature matrix of the loss function at the optimum. Its eigenvalues tell us how steep/flat the loss surface is in each direction:

Large eigenvalue = steep valley -> parameter is well-identified. Moving away a tiny-bit costs a lot.

Small eigenvalue = nearly flat region -> parameter is poorly identified. E.g. changing kappa by a lot barely moves the loss - so the optimizer just “slides along the floor”

Condition number = ratio of steepest to flattest.

The heatmap:

To see this, imagine the loss surface as a 5D bowl, not symmetric one. Each eigenvector represents a direction in the parameter space.

Each column is an eigen-direction, each row is a parameter.

Darker the color the parameter contributes more in that direction.

i.e. when the optimizer moves along that eigen-direction, that parameter is the one changing. A parameter that’s dark in a flat column (small eigenvalue) is one the data cannot control well.