11. Greeks via COS Method#

COS computes Greeks through Fourier series derivatives. We validate against BS closed-form before moving to stochastic vol.

11.1. COS Greeks Formulas#

From Fang and Oosterlee [2008], the COS option price is:

where \(H_k = \varphi\left(\frac{k\pi}{b-a}\right) e^{ik\pi\frac{x_0 - a}{b-a}}\) and \(V_k\) are payoff coefficients.

Delta - differentiate w.r.t. \(S_0\) (enters through \(x_0 = \ln(S_0/K)\)):

where \(\omega_k = \frac{k\pi}{b-a}\).

Gamma - second derivative:

Theta, Vega, Rho - computed via finite differences. Analytical formulas exist but FD is simpler and accurate enough for validation.

11.2. Point Comparison: COS vs Black-Scholes#

ATM call, standard parameters.

| BS Analytical | COS Method | Abs Error | Rel Error | |

|---|---|---|---|---|

| Greek | ||||

| price | 10.450584 | 10.450584 | 1.78e-15 | 1.70e-16 |

| delta | 0.636831 | 0.636831 | 1.54e-14 | 2.42e-14 |

| gamma | 0.018762 | 0.018762 | 1.08e-16 | 5.73e-15 |

| theta | -6.414028 | -6.415077 | 1.05e-03 | 1.64e-04 |

| vega | 37.524035 | 37.524034 | 3.04e-07 | 8.11e-09 |

| rho | 53.232482 | 53.232481 | 7.72e-07 | 1.45e-08 |

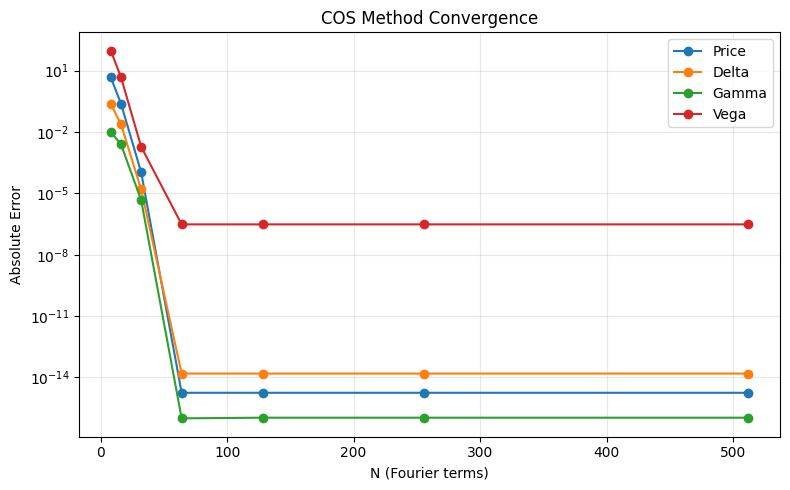

11.3. Convergence Analysis#

How does error decay as we increase the number of Fourier terms N?

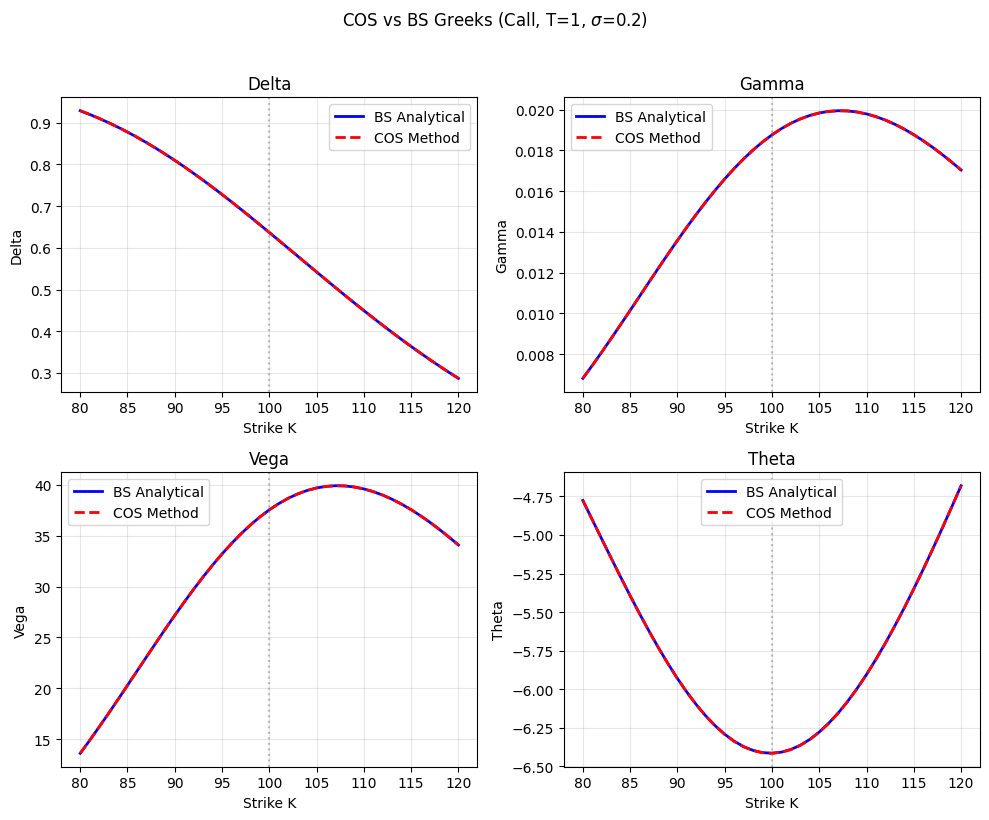

11.4. Greeks Across Strikes#

Compare COS and BS Greeks for strikes from deep ITM to deep OTM.

11.5. Interactive Comparison#

Overlay COS and BS Greeks across spot prices. Check the match holds under different parameter regimes.

COS matches BS Greeks to high precision (errors ~1e-6 for analytical, ~1e-4 for FD). Same code works for Heston or rough vol — just swap the characteristic function.