2. Exact Heston Model Simulations for Characteristic Function Methods#

2.1. Overview#

Exact simulation from Broadie and Kaya [2006]. All implementations in utils.py.

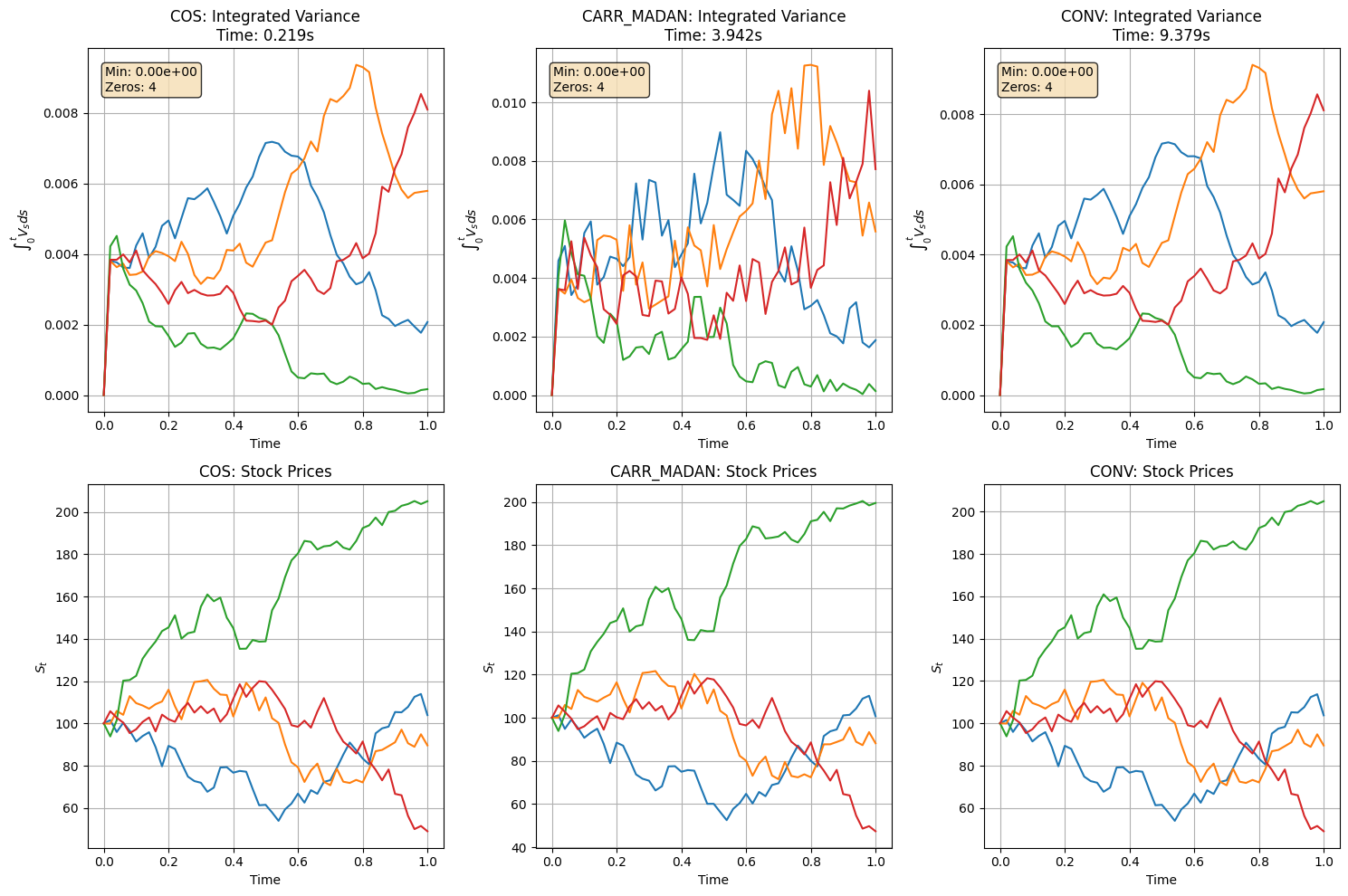

The critical step is inverting the CDF of integrated variance \(\int_0^T V_s \, ds\). We compare COS, Carr-Madan, and CONV for that inversion.

=== Testing COS Method ===

Using cos method for CDF recovery and inversion

Computation time: 0.219 seconds

Min integrated variance: 0.00000000

Values <= 1e-10: 4/204

All positive: False

=== Testing CARR_MADAN Method ===

Using carr_madan method for CDF recovery and inversion

Computation time: 3.942 seconds

Min integrated variance: 0.00000000

Values <= 1e-10: 4/204

All positive: False

=== Testing CONV Method ===

Using conv method for CDF recovery and inversion

Computation time: 9.379 seconds

Min integrated variance: 0.00000000

Values <= 1e-10: 4/204

All positive: False

=== Performance Comparison ===

COS: 0.219 seconds

CARR_MADAN: 3.942 seconds

CONV: 9.379 seconds

=== Zero Analysis ===

COS: min=0.00000000, zeros(<=1e-10)=4, exact_zeros=4

CARR_MADAN: min=0.00000000, zeros(<=1e-10)=4, exact_zeros=4

CONV: min=0.00000000, zeros(<=1e-10)=4, exact_zeros=4

Using carr_madan method for CDF recovery and inversion

Min integrated variance: 0.00000000

Zero values: 3/33

All values positive: False

First few values: [[0. 0.00820748 0.01244008 0.0057766 0.00594041]

[0. 0.01216603 0.00488742 0.00421274 0.00721754]

[0. 0.01324573 0.00684682 0.00610527 0.01005191]]

ERROR: Still seeing zeros! The fixed utils.py is not being used.

Please restart the Jupyter kernel and run all cells again.

COS is fastest since it avoids numerical integration. Carr-Madan occasionally produces near-zero PDFs that break Newton’s method — need to investigate. All three produce similar stock trajectories, the difference is in the variance sampling step.

2.2. Comparison#

COS for this application — fast, stable, no integration needed.

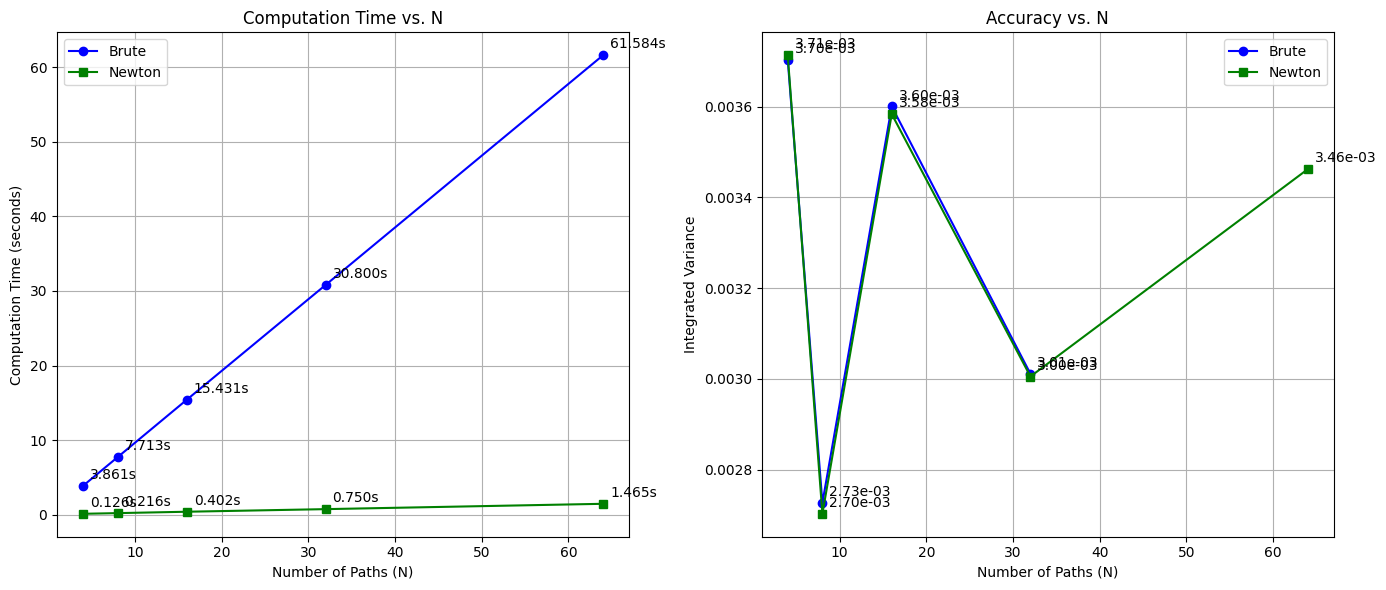

2.2.1. Newton-Raphson method vs. brute force approach for CDF inversion#

/home/runner/work/Quantitative-Finance-Book/Quantitative-Finance-Book/char_functions/../utils.py:502: RuntimeWarning: invalid value encountered in scalar multiply

chf = temp1 * temp2 * temp3 / temp4

/home/runner/work/Quantitative-Finance-Book/Quantitative-Finance-Book/char_functions/../utils.py:502: RuntimeWarning: invalid value encountered in scalar divide

chf = temp1 * temp2 * temp3 / temp4

/home/runner/work/Quantitative-Finance-Book/Quantitative-Finance-Book/char_functions/../utils.py:468: RuntimeWarning: invalid value encountered in divide

R

/home/runner/work/Quantitative-Finance-Book/Quantitative-Finance-Book/char_functions/../utils.py:479: RuntimeWarning: invalid value encountered in divide

- R * (1 + np.exp(-R * tau)) / (1 - np.exp(-R * tau))

/home/runner/work/Quantitative-Finance-Book/Quantitative-Finance-Book/char_functions/../utils.py:486: RuntimeWarning: invalid value encountered in divide

np.sqrt(vt * vu)

| N | Brute Time (s) | Newton Time (s) | vint_brute_values | vint_newton_values | |

|---|---|---|---|---|---|

| 0 | 4 | 3.860675 | 0.125718 | 0.003704 | 0.003713 |

| 1 | 8 | 7.712639 | 0.215924 | 0.002726 | 0.002702 |

| 2 | 16 | 15.431197 | 0.402222 | 0.003600 | 0.003583 |

| 3 | 32 | 30.799817 | 0.750099 | 0.003011 | 0.003005 |

| 4 | 64 | 61.583629 | 1.465462 | NaN | 0.003462 |