1. Characteristic Functions Methods Approximating CDF/PDF#

Methods implemented are based on foundational research from [].

This work builds upon advanced coursework in computational finance under Dr. Fang Fang from TU Delft.

If characteristic function is known then we can use characteristic functions (ch.f.) methods to approximate CDF and PDF. We define characteristic function of a random variable \(X\) as

\[ \varphi_X(t) = \mathbb{E}[e^{itx}] = \int_{-\infty}^{+\infty} e^{itx}f_X(x) \, \mathrm{d}x. \]where \(i\) represents the imaginary unit.

\(F_X(x)\), the cumualative distribution function (CDF) of \(X\) completely determines the characteristic function \(\varphi_X(x)\); and vice versa.

i.e. if \(X\) admist a probability density function (PDF) \(f_X(x)\), then \(\varphi_X(x)\) is its Fourier dual, in the sense that \(f_X(x)\) and \(\varphi_X(x)\) are the continuous Fourier transforms of each other.

The inversion formula; going from characteristic function to pdf $\( f_X(x) = \frac{1}{2\pi}\int_{-\infty}^{+\infty} e^{-itx}\varphi_X(t) \, \mathrm{d}t. \)$

If ch.f. of an option pricing model is known analytically or semi-analytically - for example Black-Scholes, Heston, Variance-Gamme process, Affine jump diffusion processes in general. Then, these ch.f. based methods can offer an efficient way of computing PDF by inverting the ch.f., and thus option price.

Having the corresponding PDF it allows us to price the options, i.e. computing the following integral under risk-neutral probability measure \(\mathbb{Q}\):

1.1. TO DO:#

1 - Add a summary table

---------------------------------------------------------------------------

ModuleNotFoundError Traceback (most recent call last)

Cell In[1], line 5

3 import matplotlib.pyplot as plt

4 import time

----> 5 import scipy as ss

6 from scipy.stats import norm

7 from scipy.integrate import trapezoid

ModuleNotFoundError: No module named 'scipy'

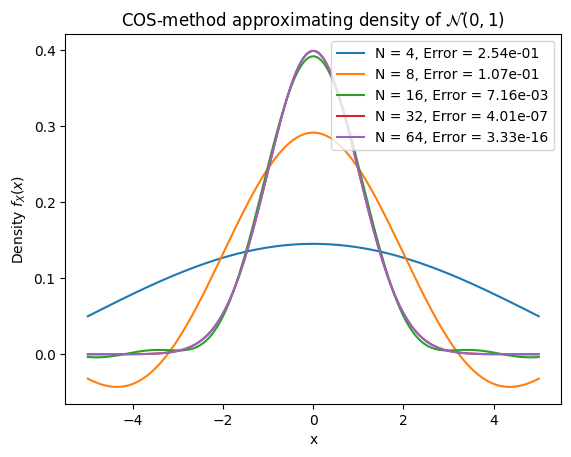

1.2. COS method#

The COS method (see Fang-Osterlee 2009) is highly efficient semi-analyitcal algorithm to solve the expectation of a function of a random variable.

Unlike FFT, COS does not require any numerical integration, thus is much faster.

For a smooth function supported on a finite interval \([a,b]\), the Fourier cosine expansion is

\[ f(x) = \frac{1}{2}A_0 + \sum^{+\infty}_{k=1} A_k \cdot \cos\left(k \pi \frac{x-a}{b-a}\right)\]So we will assume that we can make a periodic extension of the target function \(f\), by choosing an interval \([a,b]\) such that we capture the the function “well enough”.

Coefficients \(A_k\)’s can be directly sampled from the Fourier transform of \(f(x)\).

\[A_k = \frac{2}{b-a}\mathfrak{Re}\left\{ \varphi\left( \frac{k\pi}{b-a} \right)\cdot \exp\left(-i\frac{k\pi a}{b-a}\right) \right\} \]

where \(\varphi(x) = \int^a_b e^{itx}f(x) \, \mathrm{d}x\)

For a smooth probability densities \(f(x)\) supported on \((-\infty, +\infty)\) we can truncate the distribution on a large enough interval \([a, b]\) and replace \(\varphi\) in the definition of \(A_k\)’s by the characteristic function of \(f(x)\) as an accurate approximation.

COS method is proved to converge exponentially for regular densities.

To demonstrate each this,

we evaluate the equation \(f(x) = \frac{1}{\sqrt{2\pi}}e^{-1/2x^2}\),

we determine the accuracy for different values of \(N\) - number of integration points,

we choose interval \([-10, 10]\),

measure the error at \(x = \{-5, -4, \ldots, 4, 5 \}\).

# Recovery CDF

def cos_cdf(a, b, omega, chf, x):

# F_k coefficients

F_k = 2.0 / (b - a) * np.real(chf * np.exp(-1j * omega * a))

cdf = np.squeeze(F_k[0] / 2.0 * (x - a)) + np.matmul(F_k[1:] / omega[1:], np.sin(np.outer(omega[1:], x - a)))

return cdf

# Recover PDF

def cos_pdf(a, b, omega, chf, x):

# F_k coefficients

F_k = 2.0 / (b - a) * np.real(chf * np.exp(-1j * omega * a))

# Separate first term and remaining terms like in cos_cdf

pdf = F_k[0] / 2.0 + np.matmul(F_k[1:], np.cos(np.outer(omega[1:], x - a)))

return pdf

def cos_pdf2(a, b, N, chf, x): # chf(omega)

#i = np.complex(0.0, 1.0) # assigning i=sqrt(-1)

k = np.linspace(0, N-1, N)

#u = np.zeros([1,N]) # Num of arguments for ch.f.

u = k * np.pi / (b-a) # scale; frequencies -- u = omega

# F_k coefficients

F_k = 2.0 / (b - a) * np.real(chf(u) * np.exp(-1j * u * a))

F_k[0] = F_k[0] * 0.5 # first term

# Final calculation

pdf = np.matmul(F_k, np.cos(np.outer(u, x - a)))

return pdf

# Test

def generate_cos_convergence_analysis():

""" Make a plot & table of error convergence of COS method for approximating PDF of standard normal

"""

# Define characteristic function of standard normal

def chf_normal(omega):

return np.exp(-0.5 * omega**2)

# Setup test parameters

a, b = -10, 10 # Domain boundaries

x = np.linspace(-5, 5, 200) # Points to evaluate

exact_pdf = norm.pdf(x) # Exact pdf to match

N_values = [4, 8, 16, 32, 64] # Number of terms to test

# Initialise vectors

errors = []

cpu_times = []

diff_cpu_times = []

prev_time = 0

# Test each value of N

for N in N_values:

# Compute frequencies (omega) for this N

k = np.linspace(0, N-1, N)

omega = k * np.pi / (b - a)

# Pre-compute characteristic function values

chf_values = chf_normal(omega)

# Measure CPU time correctly

times = []

for _ in range(10): # Run more times for more stable timing

start = time.time()

# Use the new cos_pdf signature with pre-computed values

cos_pdf_values = cos_pdf(a, b, omega, chf_values, x)

end = time.time()

times.append((end - start) * 1000) # Convert to milliseconds

cpu_time = np.mean(times)

# Calculate maximum error

error = np.max(np.abs(cos_pdf_values - exact_pdf))

# Calculate difference in CPU time

diff_time = cpu_time - prev_time if N != 4 else 0

# Store results

errors.append(error)

cpu_times.append(cpu_time)

diff_cpu_times.append(diff_time if N != 4 else None) # Set first row = None

prev_time = cpu_time

# Plot of the approximations

plt.plot(x, cos_pdf_values, label=f'N = {N}, Error = {error:.2e}')

plt.title("COS-method approximating density of $\mathcal{N}(0,1)$")

plt.xlabel("x")

plt.ylabel("Density $f_X(x)$")

plt.legend()

plt.show()

# Create a pandas DataFrame

results_df = pd.DataFrame({

'N': N_values,

'Error': errors,

'CPU time (msec.)': cpu_times,

'Diff. in CPU (msec.)': diff_cpu_times

})

return results_df

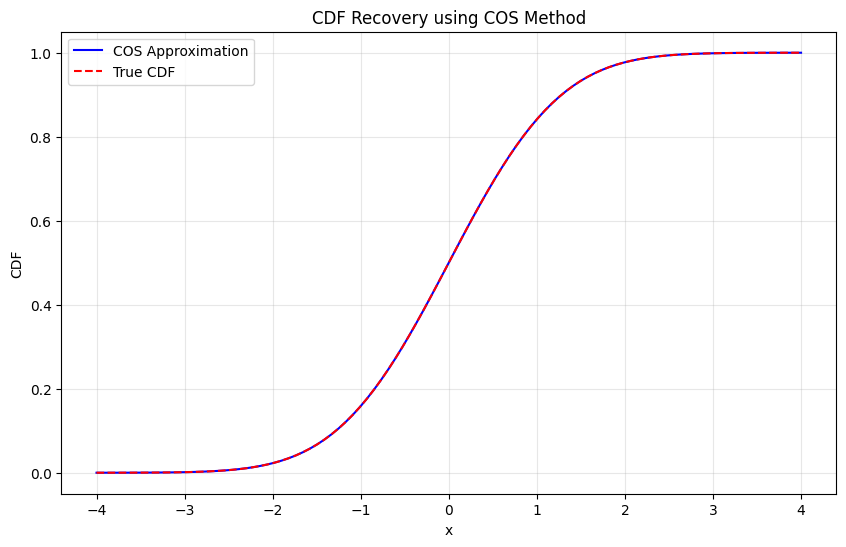

# Test COS CDF recovery

def test_cos_cdf():

""" Test CDF recovery for standard normal """

def chf_normal(u):

return np.exp(-0.5 * u**2)

x_vals = np.linspace(-4, 4, 100)

# Recover CDF

a, b, = -8.0, 8.0

N = 2**12

k_values = np.arange(N)

omega = k_values * np.pi / (b - a)

chf_values = chf_normal(omega)

cdf_approx = cos_cdf(a, b, omega, chf_values, x_vals)

# True CDF

cdf_true = norm.cdf(x_vals)

# Plot comparison

plt.figure(figsize=(10, 6))

plt.plot(x_vals, cdf_approx, 'b-', label='COS Approximation')

plt.plot(x_vals, cdf_true, 'r--', label='True CDF')

plt.title("CDF Recovery using COS Method")

plt.xlabel("x")

plt.ylabel("CDF")

plt.legend()

plt.grid(True, alpha=0.3)

plt.show()

# Report error

max_error = np.max(np.abs(cdf_approx - cdf_true))

print(f"Maximum CDF error: {max_error:.2e}")

# Run tests

if __name__ == "__main__":

print("\nConvergence table:")

print(generate_cos_convergence_analysis()) # includes the plot

print("\nTesting CDF recovery:")

test_cos_cdf()

Convergence table:

N Error CPU time (msec.) Diff. in CPU (msec.)

0 4 2.536344e-01 0.030136 NaN

1 8 1.074376e-01 0.038195 0.008059

2 16 7.158203e-03 0.022292 -0.015903

3 32 4.008963e-07 0.049615 0.027323

4 64 3.330669e-16 0.069475 0.019860

Testing CDF recovery:

Maximum CDF error: 5.55e-16

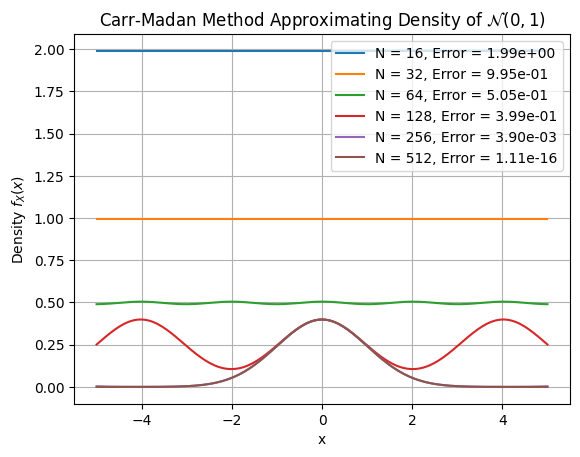

1.3. Carr-Madan method#

To demonstrate each this,

we evaluate the equation \(f(x) = \frac{1}{\sqrt{2\pi}}e^{-1/2x^2}\),

we determine the accuracy for different values of \(N\) - number of integration points,

we choose interval \([-10, 10]\),

measure the error at \(x = \{-5, -4, \ldots, 4, 5 \}\).

N_values = [16, 32, 64, 128, 256, 512]

# Recover CDF

def carr_madan_cdf(chf, x_grid, u_max=200, N=2**12):

"""

Recover CDF from characteristic function using Gil-Pelaez inversion formula.

Parameters:

- chf: function, characteristic function phi(u)

- x_grid: np.array, evaluation points for CDF

- u_max: upper frequency limit (increased for better tail accuracy)

- N: number of frequency discretization points (increased for better resolution)

Returns:

- cdf: np.array, CDF values at x_grid

"""

# Starting from close to 0

u_min = 1e-10 # Much smaller starting point to capture low-frequency behavior

u = np.linspace(u_min, u_max, N)

# Compute integrand for each x (unchanged)

integrand = np.imag(np.exp(-1j * np.outer(x_grid, u)) * chf(u)) / u # shape: (len(x), N)

# Integrate using trapezoidal rule along frequency axis (unchanged)

integral = trapezoid(integrand, u, axis=1)

# Apply Gil-Pelaez inversion formula

cdf = 0.5 - (1 / np.pi) * integral

return np.clip(np.squeeze(cdf), 0.0, 1.0) # Clamp in [0,1]

# Recover PDF

def carr_madan_pdf(chf, x_grid, u_max=100, N=2**12):

"""

Recover PDF using Carr-Madan method (Inverse Fourier Transform)

Parameters:

- chf: function, characteristic function φ(u)

- x_grid: np.array, points where to compute the PDF

- u_max: upper bound for frequency domain

- N: number of discretization points (power of 2 for FFT)

Returns:

- pdf: np.array, PDF values at each x in x_grid

"""

du = 2 * u_max / N

u = np.linspace(-u_max, u_max - du, N)

# Compute integrand of inverse Fourier transform

integrand = np.exp(-1j * np.outer(x_grid, u)) * chf(u)

# Numerical integration using trapezoidal rule

integral = np.trapezoid(integrand, u, axis=1)

pdf = np.squeeze(np.real(integral) / (2 * np.pi))

return pdf

# Test Carr-Madan

def generate_carr_madan_convergence_analysis():

""" Make a plot & table of error convergence for Carr-Madan method approximating PDF of standard normal """

def chf_normal(u):

return np.exp(-0.5 * u**2)

x = np.linspace(-5, 5, 200)

exact_pdf = norm.pdf(x)

#N_values = [16, 32, 64, 128, 256, 512] # FFT sizes

errors = []

cpu_times = []

diff_cpu_times = []

prev_time = 0

for N in N_values:

times = []

for _ in range(5): # Run a few times for stability

start = time.time()

pdf_vals = carr_madan_pdf(chf_normal, x, N=N)

end = time.time()

times.append((end - start) * 1000) # ms

cpu_time = np.mean(times)

error = np.max(np.abs(pdf_vals - exact_pdf))

diff_time = cpu_time - prev_time if N != N_values[0] else 0

errors.append(error)

cpu_times.append(cpu_time)

diff_cpu_times.append(diff_time if N != N_values[0] else None)

prev_time = cpu_time

# Plot

plt.plot(x, pdf_vals, label=f'N = {N}, Error = {error:.2e}')

plt.title("Carr-Madan Method Approximating Density of $\mathcal{N}(0,1)$")

plt.xlabel("x")

plt.ylabel("Density $f_X(x)$")

plt.legend()

plt.grid(True)

plt.show()

results_df = pd.DataFrame({

'N': N_values,

'Error': errors,

'CPU time (msec.)': cpu_times,

'Diff. in CPU (msec.)': diff_cpu_times

})

return results_df

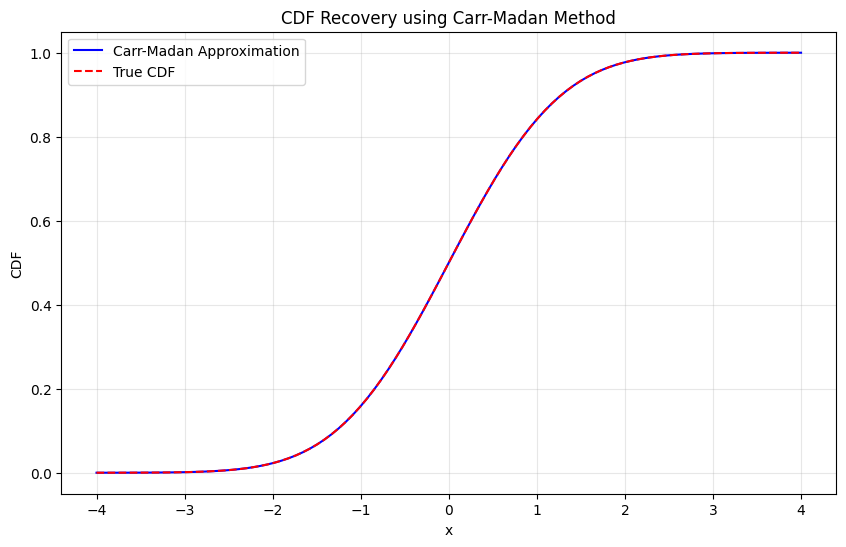

# Test Carr-Madan CDF recovery

def test_carr_madan_cdf():

""" Test CDF recovery for standard normal """

def chf_normal(u):

return np.exp(-0.5 * u**2)

x_vals = np.linspace(-4, 4, 100)

# Recover CDF

cdf_approx = carr_madan_cdf(chf_normal, x_vals, N=2**12)

# True CDF

cdf_true = norm.cdf(x_vals)

# Plot comparison

plt.figure(figsize=(10, 6))

plt.plot(x_vals, cdf_approx, 'b-', label='Carr-Madan Approximation')

plt.plot(x_vals, cdf_true, 'r--', label='True CDF')

plt.title("CDF Recovery using Carr-Madan Method")

plt.xlabel("x")

plt.ylabel("CDF")

plt.legend()

plt.grid(True, alpha=0.3)

plt.show()

# Report error

max_error = np.max(np.abs(cdf_approx - cdf_true))

print(f"Maximum CDF error: {max_error:.2e}")

# Run tests

if __name__ == "__main__":

print("\nConvergence plot and table:")

print(generate_carr_madan_convergence_analysis()) # includes the plot

print("\nTesting CDF recovery:")

test_carr_madan_cdf()

Convergence plot and table:

N Error CPU time (msec.) Diff. in CPU (msec.)

0 16 1.989435e+00 0.176573 NaN

1 32 9.947169e-01 0.168848 -0.007725

2 64 5.047621e-01 0.314140 0.145292

3 128 3.989628e-01 0.496054 0.181913

4 256 3.898076e-03 1.107597 0.611544

5 512 1.110223e-16 2.577829 1.470232

Testing CDF recovery:

Maximum CDF error: 1.27e-10

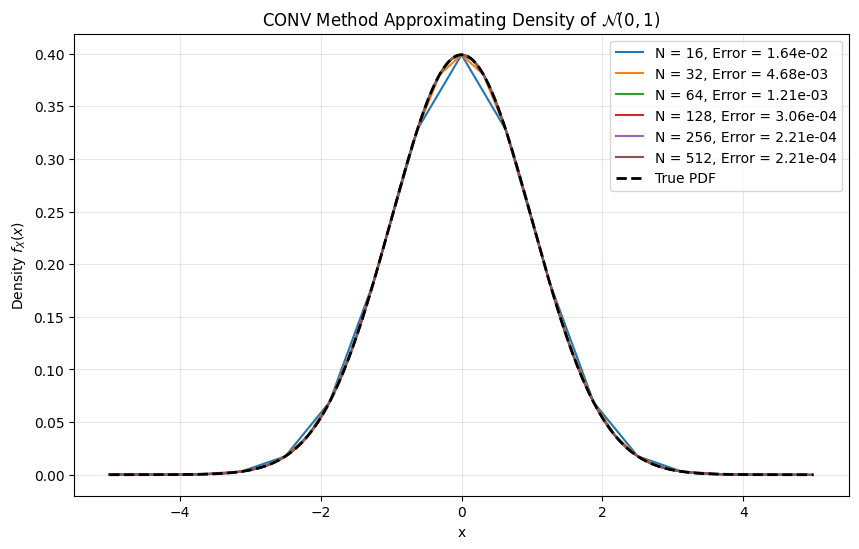

1.4. CONV method#

To demonstrate each this,

we evaluate the equation \(f(x) = \frac{1}{\sqrt{2\pi}}e^{-1/2x^2}\),

we determine the accuracy for different values of \(N\) - number of integration points,

we choose interval \([-10, 10]\),

measure the error at \(x = \{-5, -4, \ldots, 4, 5 \}\).

def conv_pdf(chf, x_range=(-5, 5), alpha=1.0, N=2**12):

"""

CONV method for PDF recovery using FFT

This implementation carefully handles the discrete approximation of:

f(x) = (1/2pi) \int phi(u-ia) e^{-iux} du

The key insights:

1. The FFT computes a discrete approximation to the continuous Fourier transform

2. We must carefully align the frequency and spatial grids

3. The damping factor 'alpha'(denote as a in comments) ensures numerical stability

Parameters:

- chf: characteristic function phi(u)

- x_range: tuple (x_min, x_max) for the output domain

- alpha: damping factor (positive for stability)

- N: number of FFT points (power of 2 recommended)

Returns:

- x: real-space grid

- pdf: corresponding recovered PDF values

"""

# Step 1: Set up the grids

x_min, x_max = x_range

L = x_max - x_min # Total length of spatial domain

# Spatial and frequency grid spacings

dx = L / N

du = 2 * np.pi / L

# Step 2: Create the frequency grid

# For FFT, we need frequencies from -u_max to u_max where u_max = pi/dx

# But FFT expects a specific ordering

u_max = np.pi / dx # Nyquist frequency

# Create frequency array in "standard" order from -u_max to u_max

if N % 2 == 0:

# For even N: [-N/2, -N/2+1, ..., -1, 0, 1, ..., N/2-1] x du

k = np.concatenate([np.arange(-N//2, 0), np.arange(0, N//2)])

else:

# For odd N: [-(N-1)/2, ..., -1, 0, 1, ..., (N-1)/2] x du

k = np.arange(-(N-1)//2, (N+1)//2)

u = k * du

# Step 3: Create the spatial grid

# Important: This grid corresponds to the FFT output ordering

x = x_min + np.arange(N) * dx

# Step 4: Evaluate the damped characteristic function

# phi(u - ia) provides exponential damping for numerical stability

phi_damped = chf(u - 1j * alpha)

# Step 5: Prepare the integrand for FFT

# We need to include a phase factor to account for the shift to x_min

# The continuous transform of phi(u)e^{-iu x_min} gives f(x + x_min)

integrand = phi_damped * np.exp(-1j * u * x_min)

# Step 6: Apply FFT with correct ordering

# FFT expects input in order [0, 1, ..., N/2-1, -N/2, ..., -1]

# So we need to reorder our frequency-domain data

integrand_fft_order = np.fft.ifftshift(integrand)

# Step 7: Compute the FFT

# This approximates the integral \int{ phi(u-ia) e^{-iu(x-x_min)} du }

fft_result = np.fft.fft(integrand_fft_order)

# Step 8: Extract and normalize the PDF

# The factor du converts the sum to an integral

# The factor 1/(2pi) comes from the inverse Fourier transform

# The factor e^{-ax} removes the damping we introduced

pdf = np.real(fft_result) * np.exp(-alpha * x) * du / (2 * np.pi)

# Step 9: Ensure non-negativity (small numerical errors can cause negative values)

pdf = np.maximum(pdf, 0)

# Check: Normalize to ensure integral equals 1

integral = trapezoid(pdf, x)

if integral > 0:

pdf = pdf / integral

return x, pdf

def conv_cdf(chf, x_vals, x_range=None, alpha=0.5, N=2**13):

"""

Recover CDF directly from characteristic function by integrating the recovered PDF.

This approach:

1. Uses conv_pdf() to recover the PDF from the characteristic function

2. Numerically integrates the PDF to get the CDF

Parameters:

- chf: characteristic function φ(u)

- x_vals: array of x values where we want to evaluate the CDF

- x_range: tuple (x_min, x_max) for PDF recovery domain

If None, automatically determined from x_vals with padding

- alpha: damping factor for PDF recovery (default 0.5)

- N: number of FFT points for PDF recovery (default 2^13)

Returns:

- cdf_vals: CDF values at the requested x_vals points

"""

# Step 1: Determine the domain for PDF recovery

if x_range is None:

# Automatically choose a domain that covers x_vals with some padding

# This ensures we capture the full probability mass

x_min_req = np.min(x_vals)

x_max_req = np.max(x_vals)

padding = (x_max_req - x_min_req) * 0.5 # 50% padding on each side

x_range = (x_min_req - padding, x_max_req + padding)

# Step 2: Recover the PDF using our existing function

x_grid, pdf_grid = conv_pdf(chf=chf, x_range=x_range, alpha=alpha, N=N)

# Step 3: Compute CDF on the native grid by cumulative integration

# Using the trapezoidal rule for integration

dx = x_grid[1] - x_grid[0] # Grid spacing (uniform)

cdf_grid = np.zeros_like(pdf_grid)

# Integrate from left to right: CDF[i] = \int_{-\infty}^{x[i]} PDF(t) dt

cdf_grid[0] = 0.0 # CDF starts at 0 at the leftmost point

for i in range(1, len(cdf_grid)):

# Add the area of the trapezoid between points i-1 and i

cdf_grid[i] = cdf_grid[i-1] + 0.5 * (pdf_grid[i-1] + pdf_grid[i]) * dx

# Alternative vectorized approach (more efficient):

# cdf_grid = np.concatenate([[0], np.cumsum(0.5 * (pdf_grid[:-1] + pdf_grid[1:]) * dx)])

# Step 4: Interpolate CDF to the requested x_vals

cdf_vals = np.interp(x_vals, x_grid, cdf_grid)

# Step 5: Ensure CDF properties are satisfied

# CDF should be between 0 and 1, and monotonically increasing

cdf_vals = np.clip(cdf_vals, 0.0, 1.0)

return cdf_vals

def conv_cdf_GP(chf, x_vals, u_max=100, N=2**13):

""" Recover CDF using Gil-Pelaez inversion formula

CDF(x) = 1/2 - (1/pi) \int_0^\infty Im[e^(-iux)phi(u)]/u du """

# Use positive u only (integrand is odd in u)

du = u_max / N

u = np.linspace(du, u_max, N) # avoid u=0 singularity

# Vectorized computation for all x values

integrand = np.imag(np.exp(-1j * np.outer(x_vals, u)) * chf(u)) / u

# Integrate over u for each x

integral = trapezoid(integrand, u, axis=1)

# Apply inversion formula

cdf = 0.5 - (1 / np.pi) * integral

return np.clip(cdf, 0.0, 1.0)

# Test functions

def plot_conv_pdf_convergence():

""" Test PDF recovery with standard normal distribution """

def chf_normal(u):

return np.exp(-0.5 * u**2)

x_true = np.linspace(-5, 5, 500)

true_pdf = norm.pdf(x_true)

#N_values = [64, 128, 256, 512, 1024, 2048]

#N_values = [16, 32, 64, 128, 256, 512]

#N_values = [4, 8, 16, 32, 64]

plt.figure(figsize=(10, 6))

# Store errors for the table

results = []

for N in N_values:

# Use fixed domain and moderate damping

x, pdf = conv_pdf(chf=chf_normal, x_range=(-5, 5), alpha=0.5, N=N)

# Interpolate to common grid for comparison

interp_pdf = np.interp(x_true, x, pdf)

error = np.max(np.abs(interp_pdf - true_pdf))

plt.plot(x, pdf, label=f'N = {N}, Error = {error:.2e}')

results.append((N, error))

plt.plot(x_true, true_pdf, 'k--', linewidth=2, label='True PDF')

plt.title("CONV Method Approximating Density of $\mathcal{N}(0,1)$")

plt.xlabel("x")

plt.ylabel("Density $f_X(x)$")

plt.legend()

plt.grid(True, alpha=0.3)

plt.show()

return results

def generate_conv_convergence_table():

""" Generate convergence table with timings """

def chf_normal(u):

return np.exp(-0.5 * u**2)

# Create a common reference grid for fair comparison

x_true = np.linspace(-5, 5, 500)

true_pdf = norm.pdf(x_true)

errors = []

cpu_times = []

diff_cpu_times = []

prev_time = 0

for N in N_values:

# Time multiple runs for accuracy

times = []

for _ in range(10):

start = time.time()

x, pdf = conv_pdf(chf=chf_normal, x_range=(-5, 5), alpha=0.5, N=N)

end = time.time()

times.append((end - start) * 1000)

avg_time = np.mean(times)

# FIXED: Interpolate to common grid before computing error

interp_pdf = np.interp(x_true, x, pdf)

error = np.max(np.abs(interp_pdf - true_pdf))

# Time difference

delta_time = avg_time - prev_time if N != N_values[0] else None

errors.append(error)

cpu_times.append(avg_time)

diff_cpu_times.append(delta_time)

prev_time = avg_time

table = pd.DataFrame({

'N': N_values,

'Error': errors,

'CPU time (msec.)': cpu_times,

'Diff. in CPU (msec.)': diff_cpu_times

})

return table

# Test CDF recovery

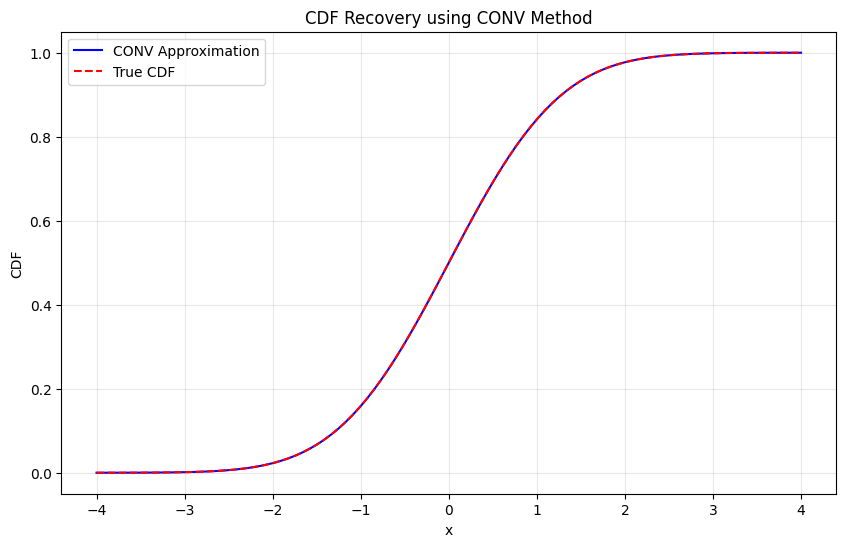

def test_conv_cdf():

""" Test CDF recovery for standard normal """

def chf_normal(u):

return np.exp(-0.5 * u**2)

x_vals = np.linspace(-4, 4, 100)

# Recover CDF

cdf_approx = conv_cdf(chf_normal, x_vals, alpha=0.5, N=2**12)

# True CDF

cdf_true = norm.cdf(x_vals)

# Plot comparison

plt.figure(figsize=(10, 6))

plt.plot(x_vals, cdf_approx, 'b-', label='CONV Approximation')

plt.plot(x_vals, cdf_true, 'r--', label='True CDF')

plt.title("CDF Recovery using CONV Method")

plt.xlabel("x")

plt.ylabel("CDF")

plt.legend()

plt.grid(True, alpha=0.3)

plt.show()

# Report error

max_error = np.max(np.abs(cdf_approx - cdf_true))

print(f"Maximum CDF error: {max_error:.2e}")

# Run tests

if __name__ == "__main__":

print("Testing PDF recovery:")

plot_conv_pdf_convergence()

print("\nConvergence table:")

print(generate_conv_convergence_table())

print("\nTesting CDF recovery:")

test_conv_cdf()

Testing PDF recovery:

Convergence table:

N Error CPU time (msec.) Diff. in CPU (msec.)

0 16 0.016440 0.047088 NaN

1 32 0.004682 0.036931 -0.010157

2 64 0.001210 0.039387 0.002456

3 128 0.000306 0.053191 0.013804

4 256 0.000221 0.047708 -0.005484

5 512 0.000221 0.120401 0.072694

Testing CDF recovery:

Maximum CDF error: 7.56e-07

def summary_convergence_table():

""" Generate convergence table with timings """

def chf_normal(u):

return np.exp(-0.5 * u**2)

# Create a common reference grid for fair comparison

x_true = np.linspace(-5, 5, 500)

true_pdf = norm.pdf(x_true)

errors = []

cpu_times = []

diff_cpu_times = []

prev_time = 0

for N in N_values:

# Time multiple runs for accuracy

times = []

for _ in range(10):

start = time.time()

# Add COS

# Add C-M

x, pdf = conv_pdf(chf=chf_normal, x_range=(-5, 5), alpha=0.5, N=N)

end = time.time()

times.append((end - start) * 1000)

avg_time = np.mean(times)

# FIXED: Interpolate to common grid before computing error

interp_pdf = np.interp(x_true, x, pdf)

error = np.max(np.abs(interp_pdf - true_pdf))

# Time difference

delta_time = avg_time - prev_time if N != N_values[0] else None

errors.append(error)

cpu_times.append(avg_time)

diff_cpu_times.append(delta_time)

prev_time = avg_time

table = pd.DataFrame({

'N': N_values,

'Error': errors,

'CPU time (msec.)': cpu_times,

'Diff. in CPU (msec.)': diff_cpu_times

})

return table

print(summary_convergence_table)

<function summary_convergence_table at 0x11fbb2a70>