2. Exact Heston Model Simuations for Characteristic Function Methods#

Here we do …

---------------------------------------------------------------------------

ModuleNotFoundError Traceback (most recent call last)

Cell In[1], line 5

3 import matplotlib.pyplot as plt

4 import time

----> 5 import scipy.special as ss

6 from scipy.stats import norm

7 from scipy.integrate import trapezoid

ModuleNotFoundError: No module named 'scipy'

# 1.ii.b - COS CDF recovery

def cos_cdf(a, b, omega, chf, x):

F_k = 2.0 / (b - a) * np.real(chf * np.exp(-1j * omega * a))

cdf = np.squeeze(F_k[0] / 2.0 * (x - a)) + np.matmul(F_k[1:] / omega[1:], np.sin(np.outer(omega[1:], x - a)))

return cdf

def cos_pdf(a, b, N, chf, x): # chf(omega)

#i = np.complex(0.0, 1.0) # assigning i=sqrt(-1)

k = np.linspace(0, N-1, N)

#u = np.zeros([1,N]) # Num of arguments for ch.f.

u = k * np.pi / (b-a) # scale; frequencies -- u = omega

# F_k coefficients

F_k = 2.0 / (b - a) * np.real(chf(u) * np.exp(-1j * u * a))

F_k[0] = F_k[0] * 0.5 # first term

# Final calculation

pdf = np.matmul(F_k, np.cos(np.outer(u, x - a)))

return pdf

# Carr-Madan

def carr_madan_cdf(chf, x_grid, u_max=200, N=2**12):

# Starting from close to 0

u_min = 1e-10 # Much smaller starting point to capture low-frequency behavior

u = np.linspace(u_min, u_max, N)

# Compute integrand for each x (unchanged)

integrand = np.imag(np.exp(-1j * np.outer(x_grid, u)) * chf(u)) / u # shape: (len(x), N)

# Integrate using trapezoidal rule along frequency axis (unchanged)

integral = trapezoid(integrand, u, axis=1)

# Apply Gil-Pelaez inversion formula

cdf = 0.5 - (1 / np.pi) * integral

return np.clip(np.squeeze(cdf), 0.0, 1.0) # Clamp in [0,1]

# Recover PDF

def carr_madan_pdf(chf, x_grid, u_max=100, N=2**12):

du = 2 * u_max / N

u = np.linspace(-u_max, u_max - du, N)

# Compute integrand of inverse Fourier transform

integrand = np.exp(-1j * np.outer(x_grid, u)) * chf(u)

# Numerical integration using trapezoidal rule

integral = np.trapezoid(integrand, u, axis=1)

pdf = np.squeeze(np.real(integral) / (2 * np.pi))

return pdf

# CONV

def conv_pdf(chf, x_range=(-5, 5), alpha=1.0, N=2**12):

# Step 1: Set up the grids

x_min, x_max = x_range

L = x_max - x_min # Total length of spatial domain

# Spatial and frequency grid spacings

dx = L / N

du = 2 * np.pi / L

# Step 2: Create the frequency grid

# For FFT, we need frequencies from -u_max to u_max where u_max = pi/dx

# But FFT expects a specific ordering

u_max = np.pi / dx # Nyquist frequency

# Create frequency array in "standard" order from -u_max to u_max

if N % 2 == 0:

# For even N: [-N/2, -N/2+1, ..., -1, 0, 1, ..., N/2-1] x du

k = np.concatenate([np.arange(-N//2, 0), np.arange(0, N//2)])

else:

# For odd N: [-(N-1)/2, ..., -1, 0, 1, ..., (N-1)/2] x du

k = np.arange(-(N-1)//2, (N+1)//2)

u = k * du

# Step 3: Create the spatial grid

# Important: This grid corresponds to the FFT output ordering

x = x_min + np.arange(N) * dx

# Step 4: Evaluate the damped characteristic function

# phi(u - ia) provides exponential damping for numerical stability

phi_damped = chf(u - 1j * alpha)

# Step 5: Prepare the integrand for FFT

# We need to include a phase factor to account for the shift to x_min

# The continuous transform of phi(u)e^{-iu x_min} gives f(x + x_min)

integrand = phi_damped * np.exp(-1j * u * x_min)

# Step 6: Apply FFT with correct ordering

# FFT expects input in order [0, 1, ..., N/2-1, -N/2, ..., -1]

# So we need to reorder our frequency-domain data

integrand_fft_order = np.fft.ifftshift(integrand)

# Step 7: Compute the FFT

# This approximates the integral \int{ phi(u-ia) e^{-iu(x-x_min)} du }

fft_result = np.fft.fft(integrand_fft_order)

# Step 8: Extract and normalize the PDF

# The factor du converts the sum to an integral

# The factor 1/(2pi) comes from the inverse Fourier transform

# The factor e^{-ax} removes the damping we introduced

pdf = np.real(fft_result) * np.exp(-alpha * x) * du / (2 * np.pi)

# Step 9: Ensure non-negativity (small numerical errors can cause negative values)

pdf = np.maximum(pdf, 0)

# Check: Normalize to ensure integral equals 1

integral = trapezoid(pdf, x)

if integral > 0:

pdf = pdf / integral

return x, pdf

def conv_cdf(chf, x_vals, x_range=None, alpha=0.5, N=2**13):

# Step 1: Determine the domain for PDF recovery

if x_range is None:

# Automatically choose a domain that covers x_vals with some padding

# This ensures we capture the full probability mass

x_min_req = np.min(x_vals)

x_max_req = np.max(x_vals)

padding = (x_max_req - x_min_req) * 0.5 # 50% padding on each side

x_range = (x_min_req - padding, x_max_req + padding)

# Step 2: Recover the PDF using our existing function

x_grid, pdf_grid = conv_pdf(chf=chf, x_range=x_range, alpha=alpha, N=N)

# Step 3: Compute CDF on the native grid by cumulative integration

# Using the trapezoidal rule for integration

dx = x_grid[1] - x_grid[0] # Grid spacing (uniform)

cdf_grid = np.zeros_like(pdf_grid)

# Integrate from left to right: CDF[i] = \int_{-\infty}^{x[i]} PDF(t) dt

cdf_grid[0] = 0.0 # CDF starts at 0 at the leftmost point

for i in range(1, len(cdf_grid)):

# Add the area of the trapezoid between points i-1 and i

cdf_grid[i] = cdf_grid[i-1] + 0.5 * (pdf_grid[i-1] + pdf_grid[i]) * dx

# Alternative vectorized approach (more efficient):

# cdf_grid = np.concatenate([[0], np.cumsum(0.5 * (pdf_grid[:-1] + pdf_grid[1:]) * dx)])

# Step 4: Interpolate CDF to the requested x_vals

cdf_vals = np.interp(x_vals, x_grid, cdf_grid)

# Step 5: Ensure CDF properties are satisfied

# CDF should be between 0 and 1, and monotonically increasing

cdf_vals = np.clip(cdf_vals, 0.0, 1.0)

return cdf_vals

def CIR_Sample(NoOfPaths, kappa, gamma, vbar, s, t, v_s):

""" Sampling from noncentral-chiSquared distribution

tau = (t - s) - time to maturity, for s<t

delta = degrees of freedom

Squared Bessel process - delta => 2, -> unique solution + 0 is not attainable!

"""

delta = 4.0 * kappa * vbar / gamma / gamma

c = 2 * kappa / (gamma ** 2 * (1 - np.exp(-kappa * (t - s))))

kappaBar = 2 * c * np.exp(-kappa * (t - s)) * v_s

sample = np.random.noncentral_chisquare(delta, kappaBar, NoOfPaths) / (2 * c)

return sample

def ChFIntegratedVariance(omega, kappa, gamma, vbar, vu, vt, tau):

""" Broadie-Kaya -> Exact sampling scheme (see paper) """

R = np.sqrt(kappa ** 2 - 2.0 * gamma ** 2 * 1j * omega)

d = 4 * kappa * vbar / gamma ** 2

temp1 = R * np.exp(-tau / 2.0 * (R - kappa)) * (1 - np.exp(-kappa * tau)) / (kappa * (1 - np.exp(-R * tau)))

temp2 = np.exp((vu + vt) / gamma ** 2 * (kappa * (1 + np.exp(-kappa * tau)) / (1 - np.exp(-kappa * tau)) - R * (1 + np.exp(-R * tau)) / (1 - np.exp(-R * tau))))

# Bessel functions

temp3 = ss.iv(0.5 * d - 1.0, np.sqrt(vt * vu) * 4.0 * R * np.exp(-R * tau / 2.0) / (gamma ** 2 * (1 - np.exp(-R * tau))))

temp4 = ss.iv(0.5 * d - 1.0, np.sqrt(vt * vu) * 4.0 * kappa * np.exp(-kappa * tau / 2.0) / (gamma ** 2 * (1 - np.exp(-kappa * tau))))

chf = temp1 * temp2 * temp3 / temp4

#chf = temp1 * temp2 * temp3 / (np.maximum(temp4, 0.01)) # fix for preventing the divBy0

return chf

2.1. Newton-Raphson method for efficient CDF inversion#

Why do we implement this? A: We want to make the pricing as fast as possible.

class CDF_Inverter:

def __init__(self, method="cos", nr_expansion=100, u_max=200, N=2**12, alpha=0.5):

self.method = method

self.nr_expansion = nr_expansion

self.u_max = u_max

self.N = N

self.alpha = alpha

def compute_cdf(self, chf, x_vals, lower_bound, upper_bound):

if self.method == "cos":

# omega array

omega = np.arange(self.nr_expansion) * np.pi / (upper_bound - lower_bound)

chf_values = chf(omega)

return cos_cdf(lower_bound, upper_bound, omega, chf_values, x_vals)

if self.method == "carr_madan":

result = carr_madan_cdf(chf, x_vals, u_max=self.u_max, N=self.N)

return np.atleast_1d(result)

elif self.method == "conv":

x_range = (lower_bound, upper_bound)

return conv_cdf(chf, x_vals, x_range=x_range, alpha=self.alpha, N=self.N)

else:

raise ValueError(f"ERROR CDF: {self.method}")

def compute_pdf(self, chf, x_vals, lower_bound, upper_bound):

if self.method == "cos":

def chf_wrapper(u):

return chf(u)

return cos_pdf(lower_bound, upper_bound, self.nr_expansion, chf_wrapper, x_vals)

elif self.method == "carr_madan":

result = carr_madan_pdf(chf, x_vals, u_max=self.u_max, N=self.N)

return np.atleast_1d(result)

elif self.method == "conv":

x_range = (lower_bound, upper_bound)

x_grid, pdf_grid = conv_pdf(chf, x_range=x_range, alpha=self.alpha, N=self.N)

return np.interp(x_vals, x_grid, pdf_grid)

else:

raise ValueError(f"ERROR PDF: {self.method}")

# Newton function for cdf inversion

def invert_cdf_newton(self, chf, lower_bound, upper_bound, p, max_iter=100, tol=1e-8):

""" 1.ii.d - Using Newton's method to find the inverse CDF

- CDF recovered by COS method (cos_cdf)

- for derivative of CDF we recover density (PDF) by COS method (cos_pdf)

"""

# Initial checks

p = max(0.0, min(1.0, p)) # Ensure p is in [0,1]

if p <= 0.0:

return lower_bound

if p >= 1.0:

return upper_bound

# Evaluate CDF at a few points to provide better initial guess

# For 20 - few issues in IntVar hitting 0

# For 25 - hits fewer 0s

# For 50 - seems good

# Sweetspot = around 30

# Will depend on the params chosen for Heston; ie kappa, gamma, vbar, v0

initial_points = 30

x_initial = np.linspace(lower_bound, upper_bound, initial_points)

#cdf_initial = cos_cdf(lower_bound, upper_bound, omega, chf, x_initial) # Evaluade cdf at 30 points

cdf_initial = self.compute_cdf(chf, x_initial, lower_bound, upper_bound) # Evaluade cdf at 30 points

# Find closest point to target probability

idx = np.abs(cdf_initial - p).argmin() # Pick the closes

x = x_initial[idx] # Initial guess "best"

# Newton-Raphson iteration

for i in range(max_iter):

# Calculate CDF at current point

cdf_x = self.compute_cdf(chf, np.array([x]), lower_bound, upper_bound)[0]

# Calculate distance from target f(x) = CDF(x) - p

fx = cdf_x - p

# Check: If |F(x) - p| < tol.

if abs(fx) < tol:

return x

# Calculate F'(x) = PDF at current point using cos_pdf

pdf_x = self.compute_pdf(chf, np.array([x]), lower_bound, upper_bound)[0]

# Safeguard against division by very small numbers

if abs(pdf_x) < 1e-10:

pdf_x = 1e-10 if pdf_x >= 0 else -1e-10

# Update using Newton step

x_new = x - fx / pdf_x

# Keep within bounds

x_new = max(lower_bound, min(upper_bound, x_new))

# Check for convergence

if abs(x_new - x) < tol:

return x_new

# Update for next iteration

x = x_new

return x

def GeneratePathsHestonES(NoOfPaths, NoOfSteps, T, r, S_0, kappa, gamma, rho, vbar, v0, nr_expansion, L,

recovery_method="cos", **method_kwargs):

""" Exact Simulation - exact sampling from the non-central chi-squared distribution

"brute" - initially provided brute force approach;

"newton" - newton method (default) """

dt = T / float(NoOfSteps)

p = np.random.uniform(0, 1, [NoOfPaths, NoOfSteps]) # cdf_inversion_newton tries to find this p

Z1 = np.random.normal(0.0, 1.0, [NoOfPaths, NoOfSteps])

V = np.zeros([NoOfPaths, NoOfSteps + 1])

V_int = np.zeros([NoOfPaths, NoOfSteps + 1])

X = np.zeros([NoOfPaths, NoOfSteps + 1])

V[:, 0] = v0

V_int[:, 0] = v0 * dt

X[:, 0] = np.log(S_0)

time = np.zeros([NoOfSteps + 1])

# Initialise the CDF_Inverter with the method of choice

inverter = CDF_Inverter(method=recovery_method, nr_expansion=nr_expansion, **method_kwargs)

print(f"Using {recovery_method} method for CDF recovery and inversion")

for i in range(0, NoOfSteps):

# making sure that samples from normal have mean 0 and variance 1

if NoOfPaths > 1:

Z1[:, i] = (Z1[:, i] - np.mean(Z1[:, i])) / np.std(Z1[:, i])

# STEP 1: Exact samles for the variance process

V[:, i + 1] = CIR_Sample(NoOfPaths, kappa, gamma, vbar, 0, dt, V[:, i])

# STEP 2: Generate a sample from the distribution of the integrated variance process

# We will first have to find a bound on which we want to compute our distribution. We can do this using the

# relation between the second moment and the second derivative of the characteristic function at w = 0. We use

# a finite difference approximation.

for j in range(0, NoOfPaths):

chf_omega = lambda w: ChFIntegratedVariance(w, kappa, gamma, vbar, V[j, i], V[j, i + 1], dt) # dt = tau! Here does NoOfSteps come in

first_moment = -1j * (chf_omega(dt) - 1) / dt

second_moment = -1 * (chf_omega(2 * dt) - 2 * chf_omega(dt) + 1) / (dt ** 2)

standard_deviation = np.sqrt(abs(second_moment) - abs(first_moment) ** 2)

# standard_deviation = np.sqrt(variance)

# Lower bound of the variance process is 0, the upperbound we will take L * standard deviation.

lower_bound = 0

upper_bound = abs(first_moment) + L * standard_deviation

V_int[j, i + 1] = inverter.invert_cdf_newton(chf_omega, lower_bound, upper_bound, p[j, i])

# STEP 3: Recover a sample from the expression of the Ito integral using the solution of the CIR process

ito_integral_Ws1 = 1.0 / gamma * (V[:, i + 1] - V[:, i] - kappa * vbar * dt + kappa * V_int[:, i])

# ito_integral_Ws1 = 1.0 / gamma * (V[:, i + 1] - V[:, i] - kappa*(vbar - V_int[:, i])*dt

# STEP 4: Generate a sample of St

m = X[:, i] + (r * dt - 1.0 / 2.0 * V_int[:, i] + rho * ito_integral_Ws1)

variance = (1 - rho ** 2) * V_int[:, i]

X[:, i + 1] = m + np.sqrt(variance) * Z1[:, i]

time[i + 1] = time[i] + dt

# Compute exponent

S = np.exp(X)

paths = {"time": time, "S": S, "Vint": V_int}

return paths

if __name__ == "__main__":

# Parameters

NoOfPaths = 4

NoOfSteps = 50

# Heston model parameters

gamma = 0.4 # vol of vol

kappa = 0.5 # speed of mean reversion

vbar = 0.2 # long-term mean

rho = -0.9 # negativ correlation

v0 = 0.2 # initial variance

T = 1.0

S_0 = 100.0

r = 0.1

nr_expansion = 100

L = 10

# Set random seed for reproducibility

np.random.seed(3)

# Test all three methods

methods_to_test = {

"cos": {},

"carr_madan": {"u_max": 200, "N": 2**12},

"conv": {"alpha": 0.5, "N": 2**13}

}

results = {}

for method_name, kwargs in methods_to_test.items():

print(f"\n=== Testing {method_name.upper()} Method ===")

# Reset random seed to ensure fair comparison

np.random.seed(3)

start_time = time.time()

paths = GeneratePathsHestonES(

NoOfPaths, NoOfSteps, T, r, S_0, kappa, gamma, rho, vbar, v0,

nr_expansion=nr_expansion, L=L, recovery_method=method_name, **kwargs

)

end_time = time.time()

results[method_name] = {

"paths": paths,

"computation_time": end_time - start_time

}

print(f"Computation time: {end_time - start_time:.3f} seconds")

# Plot comparison

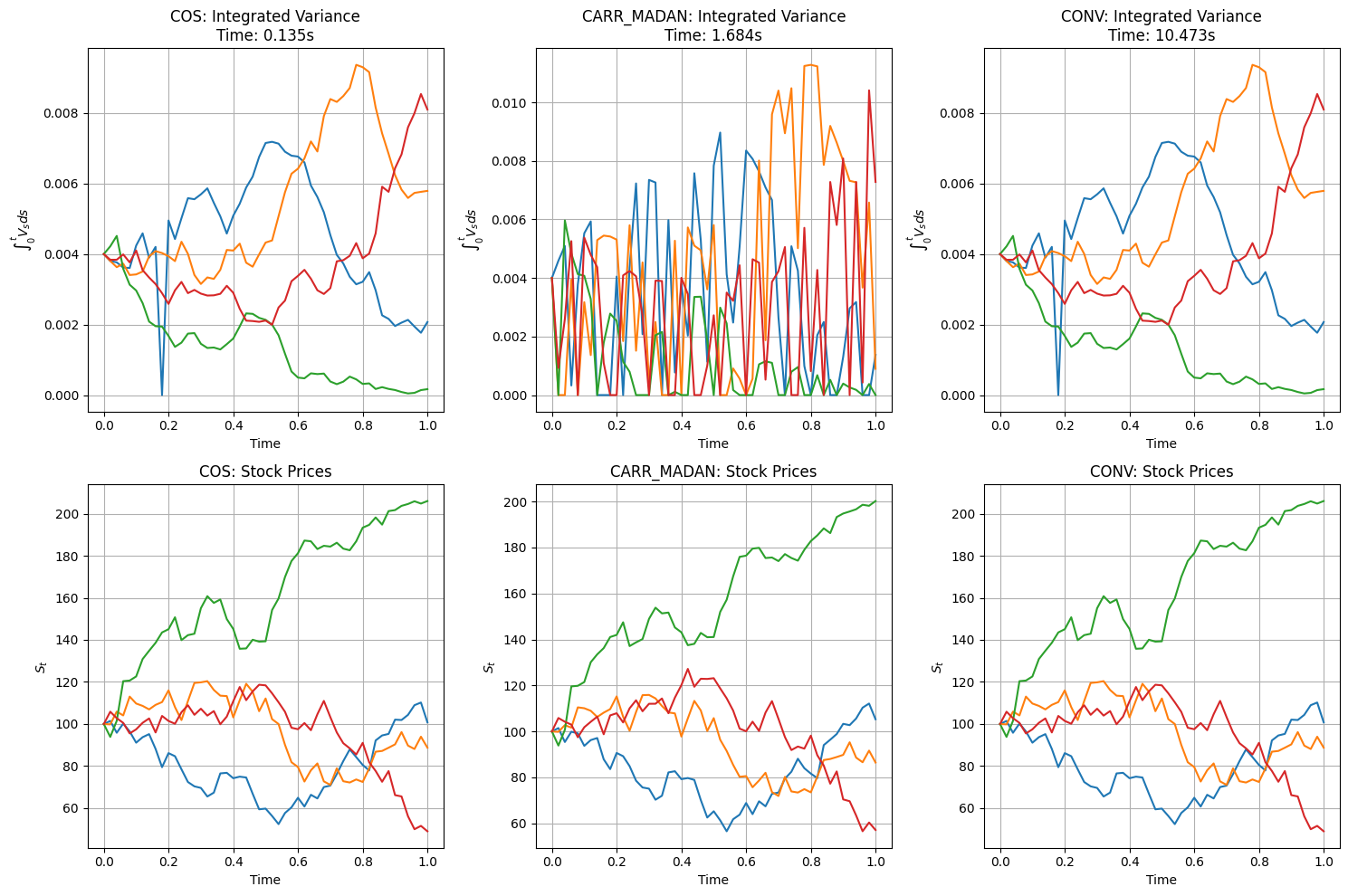

fig, axes = plt.subplots(2, 3, figsize=(15, 10))

for idx, (method_name, result) in enumerate(results.items()):

timeGrid = result["paths"]["time"]

S = result["paths"]["S"]

V_int = result["paths"]["Vint"]

# Plot integrated variance

axes[0, idx].grid(True)

axes[0, idx].plot(timeGrid, np.transpose(V_int))

axes[0, idx].set_xlabel('Time')

axes[0, idx].set_ylabel(r'$\int_0^t V_s ds$')

axes[0, idx].set_title(f'{method_name.upper()}: Integrated Variance\nTime: {result["computation_time"]:.3f}s')

# Plot stock price paths

axes[1, idx].grid(True)

axes[1, idx].plot(timeGrid, np.transpose(S))

axes[1, idx].set_xlabel('Time')

axes[1, idx].set_ylabel(r'$S_t$')

axes[1, idx].set_title(f'{method_name.upper()}: Stock Prices')

plt.tight_layout()

plt.show()

# Print timing comparison

print("\n=== Performance Comparison ===")

for method_name, result in results.items():

print(f"{method_name.upper()}: {result['computation_time']:.3f} seconds")

=== Testing COS Method ===

Using cos method for CDF recovery and inversion

Computation time: 0.135 seconds

=== Testing CARR_MADAN Method ===

Using carr_madan method for CDF recovery and inversion

Computation time: 1.684 seconds

=== Testing CONV Method ===

Using conv method for CDF recovery and inversion

Computation time: 10.473 seconds

=== Performance Comparison ===

COS: 0.135 seconds

CARR_MADAN: 1.684 seconds

CONV: 10.473 seconds

2.2. Observations#

1 COS and CONV seems to work well.

2 Integrated variance process hits zeros for Carr-Madan method

/var/folders/1p/dh14fkh53hddc1l6713y6pmm0000gn/T/ipykernel_90442/2954915863.py:28: RuntimeWarning: invalid value encountered in scalar multiply

chf = temp1 * temp2 * temp3 / temp4

/var/folders/1p/dh14fkh53hddc1l6713y6pmm0000gn/T/ipykernel_90442/2954915863.py:28: RuntimeWarning: invalid value encountered in scalar divide

chf = temp1 * temp2 * temp3 / temp4

/var/folders/1p/dh14fkh53hddc1l6713y6pmm0000gn/T/ipykernel_90442/2954915863.py:19: RuntimeWarning: invalid value encountered in divide

temp1 = R * np.exp(-tau / 2.0 * (R - kappa)) * (1 - np.exp(-kappa * tau)) / (kappa * (1 - np.exp(-R * tau)))

/var/folders/1p/dh14fkh53hddc1l6713y6pmm0000gn/T/ipykernel_90442/2954915863.py:21: RuntimeWarning: invalid value encountered in divide

temp2 = np.exp((vu + vt) / gamma ** 2 * (kappa * (1 + np.exp(-kappa * tau)) / (1 - np.exp(-kappa * tau)) - R * (1 + np.exp(-R * tau)) / (1 - np.exp(-R * tau))))

/var/folders/1p/dh14fkh53hddc1l6713y6pmm0000gn/T/ipykernel_90442/2954915863.py:24: RuntimeWarning: invalid value encountered in divide

temp3 = ss.iv(0.5 * d - 1.0, np.sqrt(vt * vu) * 4.0 * R * np.exp(-R * tau / 2.0) / (gamma ** 2 * (1 - np.exp(-R * tau))))

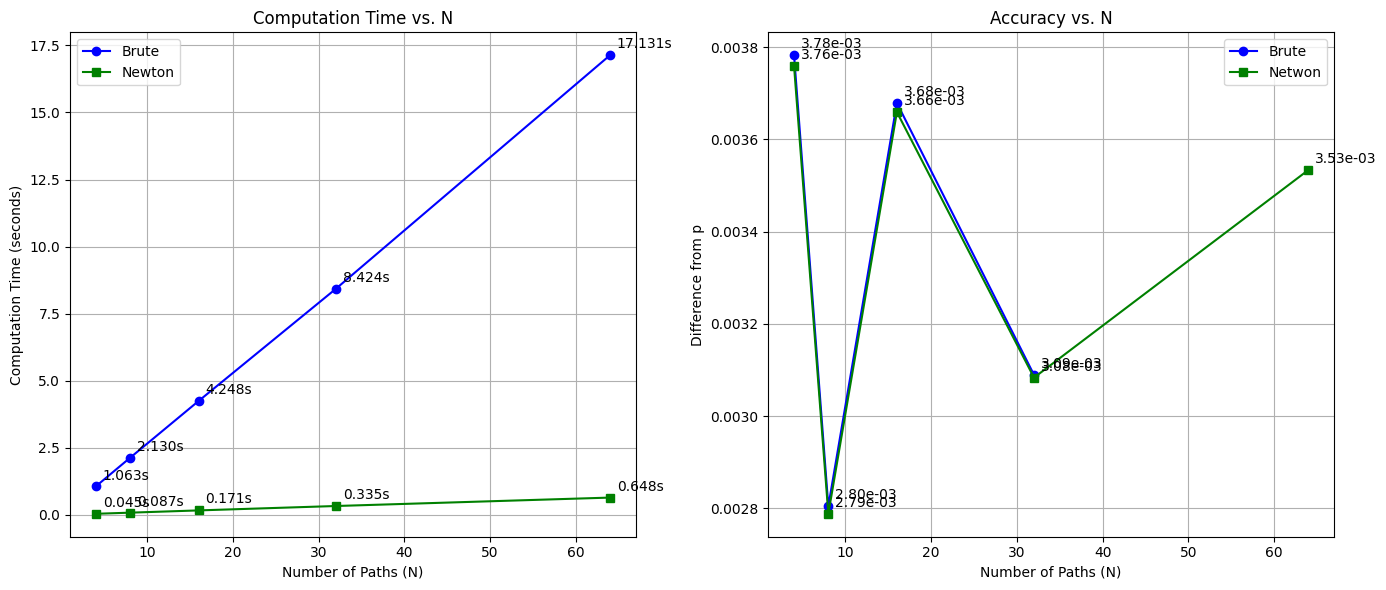

| N | Brute Time (s) | Newton Time (s) | vint_brute_values | vint_newton_values | |

|---|---|---|---|---|---|

| 0 | 4 | 1.063372 | 0.044553 | 0.003782 | 0.003759 |

| 1 | 8 | 2.130005 | 0.086690 | 0.002805 | 0.002788 |

| 2 | 16 | 4.247537 | 0.170797 | 0.003679 | 0.003659 |

| 3 | 32 | 8.423634 | 0.334534 | 0.003089 | 0.003083 |

| 4 | 64 | 17.131139 | 0.648479 | NaN | 0.003533 |